Best Intrinsic Value Formulas for Small Investors

Introduction

Understanding intrinsic value formulas is vital for successful investing. It is possible to buy the greatest company in the world but if you pay too high of a price it is going to lead to a bad investment, price matters.

Numerous intrinsic value formulas can be utilized when investing so it sometimes feels a bit overwhelming. No one intrinsic value formula fits all situations so determining the right formula requires a value judgment. You need to determine the best intrinsic value formula to use when assessing the value of the company being analyzed.

The intrinsic value of a company is a term that is used a lot in value investing circles, but what is it and how can it help with your investments? We will run through a few examples of different intrinsic value formulas - discount based, multiple-based, and asset-based approaches. We will also put them into practice and discuss some problems as well as some of the advantages of each.

What is Intrinsic Value?

In basic terms, intrinsic value tells you what the stock is currently worth, the true worth of an asset (business, stock, debt, etc).

Warren Buffett defines intrinsic value as follows:

“Intrinsic value is an all-important concept that offers the only logical approach to evaluating the relative attractiveness of investments and businesses. Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.”

- Warren Buffett, Page 4 of his Owner’s Manual

He goes on to add:

“The calculation of intrinsic value, though, is not so simple. As our definition suggests, intrinsic value is an estimate rather than a precise figure, and it is additionally an estimate that must be changed if interest rates move or forecasts of future cash flows are revised. Two people looking at the same set of facts, moreover – and this would apply even to Charlie and me – will almost inevitably come up with at least slightly different intrinsic value figures. That is one reason we never give you our estimates of intrinsic value. What our annual reports do supply, though, are the facts that we ourselves use to calculate this value.”

- Warren Buffett, Page 4 of his Owner’s Manual

Warren Buffett’s mentor, Benjamin Graham first introduced the concept of intrinsic value within Security Analysis which laid the foundations of fundamental analysis. Graham indicates that intrinsic value is:

“...that value which is justified by the facts…”

- Ben Graham, Security Analysis (1951 Edition)

The quote goes on to state that the facts are the assets, earnings, and dividends. The Benjamin Graham quote appears easier to understand but as Buffett shows, there is more to intrinsic value then Graham’s simplicity indicated.

Benjamin Graham indicates that before making any stock purchase you must know the intrinsic value of the company and only buy when the stock price is less than the market value. This same principle applies in reverse - when intrinsic values rise above the market value you should sell and take your profits.

As an investor, Graham teaches, it is important to buy and hold until mean reversion takes its course. Mean reversion is a theory that over time the market price and intrinsic value will converge until the stock price reaches its true value, this is a key component to Benjamin Graham’s intrinsic value approach to investing. This true value is a company’s intrinsic value which can be arrived at with several formulas which we will discuss below.

Starting to understand intrinsic value is an important process in the education of a value investor, what is equally important is knowing how to apply and calculate it.

Discounted Cash Flow Intrinsic Value Formulas

A discounted cash flow (DCF) the first of the intrinsic value formulas is a valuation method used to estimate the value of an investment based upon its future cash flows. This is an important valuation method to understand the value of the entire company. It is based on the idea that an investment is worth the cash you can get from it discounted back at an appropriate rate to today.

There exist within the DCF intrinsic value formula some fatal flaws that can lead to vastly different outcomes when valuing a company. These flaws can be detrimental to your investment returns and need to be understood. We will discuss these ahead.

Imagine for a moment you are the owner of an entire company and get to keep all of the future cash flows, a DCF will help you to figure out how much those cash flows are worth today.

On the other hand, a Dividend Discount Model (DDM) is used by investors to figure out and measure the intrinsic value of a stock based upon the totality of the future income received from the company’s dividend discounted back at an appropriate rate to today. A dividend represents the income received from a company’s excess cash and is comparable with coupon payments received on bonds.

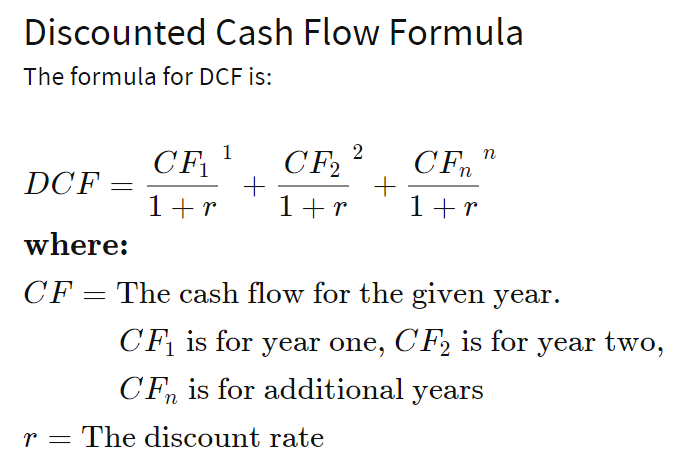

How to Calculate Intrinsic Value of a Stock Using Discounted Cash Flow

The DCF intrinsic value formula is as follow:

As it can be seen a somewhat complex looking formula, but when it is broken down and practiced like most things it does become easier. The DCF formula can be broken down into four elements:

- Discount rate - how much you would earn if you invested in another investment with similar risk

- Projected cash flow - projected to occur annually

- Periods of time - the time the analysis covers and;

- Terminal value - the growth rate for future years outside of the period covered

It might now be time to work through an example to put the theory into practice. First step: estimate the future cash flows of the company by using a free cash flow formula, such as:

EBIT – Taxes + Depreciation & Amortization – Capital Expenditures – increases in non-cash working capital = Free Cash Flow

In this example let's say the company’s cash flow last year was $25 million.

Next, determine the company’s growth rate by comparing the previous year’s cash flow ($25 million) with earlier years. The company is estimated to grow at 5% for the first two years and 2% for the following three years.

The final part is the terminal value percentage which is the company’s long term growth rate. The growth rate in the U.S for mature companies is around 3% so this can be used as a starting point.

With the above, it is now possible to calculate the projected cash flow for each year.

Year 1 - 25 * 1.05 = 26.25

Year 2 - 26.25 * 1.05 = 27.56

Year 3 - 27.56 * 1.02 = 28.11

Year 4 - 28.11 * 1.02 = 28.67

Year 5 - 28.67 * 1.02 = 29.24

Terminal Value - 29.24 (1.03) / (0.04 - 0.03) = 2393.72

The next step is to discount these future cash flows back to today by the company’s weighted average cost of capital. There is a separate equation for working this out which is beyond the scope of this piece but it is a figure that is sometimes published within the company’s annual report. If not and are in doubt you can use a default rate of 10%. In this example, the company’s discount rate is 4% which would result in company value of $2.09 billion.

If you are interested here is the math:

(26.25 / 1.041)

+(27.56 / 1.042)

+(28.11 / 1.043)

+(28.67 / 1.044)

+(29.24 / 1.045)

+(2393.72 / 1.045)

25.24

+25.48

+24.99

+24.51

+24.03

+1967.46

2,091.71

As an investor, if you were to pay less than the $2.09 billion for the company, your rate of return would be higher than the discount rate. In this example, you would not be receiving a great return on your investment unless you were to pay significantly less than the value derived from the DCF analysis. To get the per-share value, just divide the value by the number of shares outstanding.

The DDM intrinsic value formula otherwise known as the Gordon Growth Model is as follows:

Stock Price= (dividend payment in the next period)/ (cost of equity-dividend growth rate)

With the DDM intrinsic value formula, if the present stock value is higher than a stock’s market value, this indicates that the stock is undervalued and is a potential buy.

As an example, if a company declares a dividend of $2 per share and has been priced by the market at $125 an investor can estimate the intrinsic value of the company by using a DDM. By looking at the stock dividend history you can work out the dividend growth rate, in this example say 5% and in this instance, you determine a discount rate of 7%. The present stock value based upon a DDM can be worked out as follows:

Present Stock Value = $2.00 per share / (0.07 discount rate - 0.05 dividend growth) = $2.00 / 0.02 = $100.

Therefore with a present value of $100 against a market value of $125 the stock is overvalued and represents a selling opportunity. As can be seen, this is a simple method in comparison to a DCF but as outlined below there are a few critical issues with each of these intrinsic value formulas.

Problems and Advantages of Discount Models for Calculating Intrinsic Value

On a more positive note, a DFC is claimed can be said to capture the underlying fundamental drivers of business value (weighted average cost of capital, growth rate, etc.). As such, it comes pretty near to estimating the intrinsic value of the business when accurate. Unfortunately, that last caveat proves a deal breaker for all but the most gifted investors.

The main problem with the DCF is that it needs the investor to make two risky assumptions. Firstly, future cash flows need to be correctly estimated and projected out over several years. This is notoriously difficult to do as future cash flow depends on factors that change quickly over time, causing the model to be inaccurate. If estimated cash flows are too high, this could result in overvaluing the company, resulting in a poor investment, a potentially costly mistake, or a missed investment opportunity.

Secondly, the discount rate also needs to be estimated correctly for the model to be remotely accurate. Small changes in the discount rate end up having a very large impact on your resulting valuation.

It is also important to remember that the map is not the territory, the model is just that, a model. The DCF only represents an estimate of future cash flows and the value of a business.

The DDM is similar in that it requires the investor to make several assumptions, such as the growth rate, the required rate of return (discount rate), and the tax rate. It is also based upon a flawed assumption that the value of a stock is only achieved through the return on investment received through dividends.

In addition, it may seem obvious but the DDM cannot be used for evaluating a stock that doesn’t pay a dividend. Those stock buybacks, which can affect the value received by the shareholders throughout ownership, and business growth play no role in this intrinsic value formula.

Still, the DDM is a commonly used model and relatively easy to understand. It helps to eliminate in part the external market conditions so make it easier to carry out comparisons across industries and companies of different market caps.

Multiple-based Valuation - P/E & P/CF

Multiple-based intrinsic value approaches are substantially easier to use for real world investing, so it’s worth diving into two of the most common.

The Price/Earnings (P/E) ratio values a company based upon its share price relative to its per-share earnings (EPS). It indicates the dollar amount an investor pays in order to receive a dollar of the company’s earnings. A P/E of 20x, for example, indicates that an investor would have to pay $20 for $1 of earnings.

A high P/E ratio typically indicates that a company is expensive or overvalued or that there are high expectations for the future of the company. Similarly, a low P/E ratio suggests that the firm is undervalued or that earnings may not prove robust.

Multiple approaches, and especially the P/E approach, is widely used for gaging how a stock measures up against its industry peer group or a benchmark, such as the S&P 500. In our experience, this can prove a very flawed approach, however. More ahead.

The Price to cash flow ratio (P/CF) also evaluates the price of a company’s stock relative to its cash flow, typically on a per share basis. For the best results with this approach, it is best to use a company’s free cash flow, cash flow from operations, less maintenance capital expenditures. Although it will take more time, it will result in a more accurate outcome.

Again, the resulting multiple is often used for comparison sake, and with similar flaws. The multiple-based approaches are comparable measures of value but are best used in conjunction with another intrinsic value formula.

How to Calculate Intrinsic Value of a Stock Using a Multiple-based Intrinsic Value Formula

The P/E is a fairly easy ratio to calculate, take the market price per share of the company, and divide it by the earnings per share (EPS). For example company XYZ has an EPS of $2.61, and a share price of $24.57. The P/E would therefore equal $24.57/$2.61 = $9.41.

As such, company XYZ has a P/E of 9.41. In isolation this doesn’t really tell you all that much, you would need to compare this to a benchmark or industry to understand the relative value. The S&P 500 has an average P/E of 15, therefore the company would be considered undervalued relative to the S&P 500, simple!

Problems and Benefits With the Multiple-based Approach to Assessing Fair Value

The simplicity of these valuation techniques is both a problem and an advantage. Simple multiples allow investors to make quick comparisons of company value. These techniques simplify complex information into a single value, discarding other valuable factors that affect the intrinsic value, such as a company’s growth or decline. These factors have a major impact on the value of companies and meaningfulness of their output.

Multiples are also easily manipulated and misinterpreted with comparisons not really being conclusive. Earnings, for example, can be misstated, and are impacted by accounting decisions. At least with P/CF, when using free cash flow, it is less easily manipulated. These valuation multiples are also static - they exclude the future growth of a company from the equation - and exclude net cash levels. In the end, all multiple-based valuation methods are a “quick and dirty” approach and should be used in conjunction with another valuation technique.

Asset and Liquidation Based Valuations Offer a Conservative and Practical Set of Intrinsic Value Formulas

An assets-based intrinsic value formula is, you guessed it, a valuation method based upon the value of the company’s assets.

The best approach to finding intrinsic value based on assets is the net current asset value (NCAV) formula. NCAV was Benjamin Graham’s preferred intrinsic valuation formula, who dubbed stocks that met his strict criteria, net nets.

The formula can be defined as NCAV = Current Assets - Total Liabilities - Preferred Shares - Off-Balance Sheet Liabilities

NCAV is a rough indication of the company’s real world liquidation value, it helps to estimate how much cash an investor could receive if the operations were stopped, creditors paid off and assets sold. This is a highly conservative method for estimating company value, and a very effective approach to investing. Given the conservative nature of this valuation method, it tends to underestimate the company value as opposed to overstating which works in the investor’s favor.

Asset-based valuation methods such as NCAV or net tangible asset value can be used in part as a floor price for a company or as a way to value assets not reflected within another valuation approach. However, this characterization sells these measures somewhat short since quality opportunities trading below their NCAV have performed very well over the long term.

How to Calculate the Intrinsic Value of a Stock Using the Net Current Assets Intrinsic Value Formula

If a company’s current assets are $100 per share and total liabilities (Including Off Balance Sheet Liabilities) plus any preferred share value is $40 per share, net current asset value would be $60 per share.

Let’s take a look through another example to help cement this concept. Head over to the balance sheet of the company you are researching and look for the total current assets. In this example, the total current assets are $24 million. Next, look at the total liabilities (in this case, long-term debt, preferred stock, and unfunded pension liabilities), for this imagined company which equals $17 million. The firm’s NCAV amounts to $7 million. Now, divide this by the number of shares outstanding, which are 22 million in this case, and the per-share net-net value would equal $0.32. If the company’s share price is less than that, it’s a net net.

This is a simplified example but helps to illustrate the point, you would likely have to dig into the company’s financial footnotes to find all of the off-balance sheet liabilities but hopefully, this helps to illustrate the methodology.

Problems and Benefits with Asset-based Approaches to Assessing Fair Value

As has been the case with the other valuation approaches, it's time to discuss the problems and benefits with asset-based approaches. For starters, they don’t incorporate the actual cash that can be generated from the business, nor does it take into account the growth rates. However, by ignoring the possible growth, nevermind earnings, an investor can achieve large returns when growth does happen.

In addition, once you have carried out a few asset-based intrinsic valuations, it is a fairly simple process that provides a good indication as to the liquidation value of the company. It should however be emphasized that this approach results in a good approximate real world liquidation value only and not an exact value for the company.

Again, liquidation value is a hyper-conservative method that has been associated with some of the highest returns available for small investors. Graham earned 20% for thirty years investing in net nets, while Warren Buffett earned a 30% yearly return for 13 years during his partnership days and was the route that led to him becoming a millionaire.

Which Value Investing Formula is Best for You?

There are numerous intrinsic value formulas that investors can use to understand the value of the company. Each method has its problems, advantages, and levels of complexity for applying them to company valuation.

All of the intrinsic value methods discussed are valid and useful in their own right. However, the NCAV formula is a very useful tool for investors to identify groups of stocks that are probably undervalued and my favored approach. Among that group, investors should apply additional criteria to identify the real bargains and avoid value traps. I use Net Net Hunter for that exact purpose. The monthly shortlist members receive is a great place to start looking for high-quality net-nets -- and I’ve found quite a few!

Click here to get FREE net net stock checklist.

Article Author: Phillip Richards

Article image (Creative Commons) by Nana B Agyei, edited by Net Net Hunter.