Net Tangible Assets: Your Essential Stock Guide

Get full access to our VIP Newsletter right now, for FREE. Click Here.

Buying stocks at discounts to net tangible assets value has proven itself as a winning strategy time and time again.

Studies have found annual returns for a group of these bargains are around 25% in the long run.

Famous value investors like Warren Buffett — in his early years — Walter Schloss and Peter Cundill trounced the indexes for decades through expanding their portfolio by buying stocks for prices below net tangible assets value.

Assessing this kind of stocks can be tricky, though. You have to be able to distinguish tangible from intangible assets on the balance sheet, as well as familiarize yourself with some accounting rules that are far from intuitive.

Lucky for you, in this article, we’ll walk you through these concepts in depth.

While buying stocks at discounts to net tangible assets is profitable, we'll also discuss an even more profitable strategy here. But first, let’s talk about book value.

Net Tangible Assets: Building on Book Value

Some value investors use book value as a rough measure of intrinsic value. However, this measure has its limitations, as you'll see in a moment.

What is Book Value?

Book value (BV) is the net value of a company’s assets — i.e., the value of total assets less total liabilities on the balance sheet.

But that figure can be misleading.

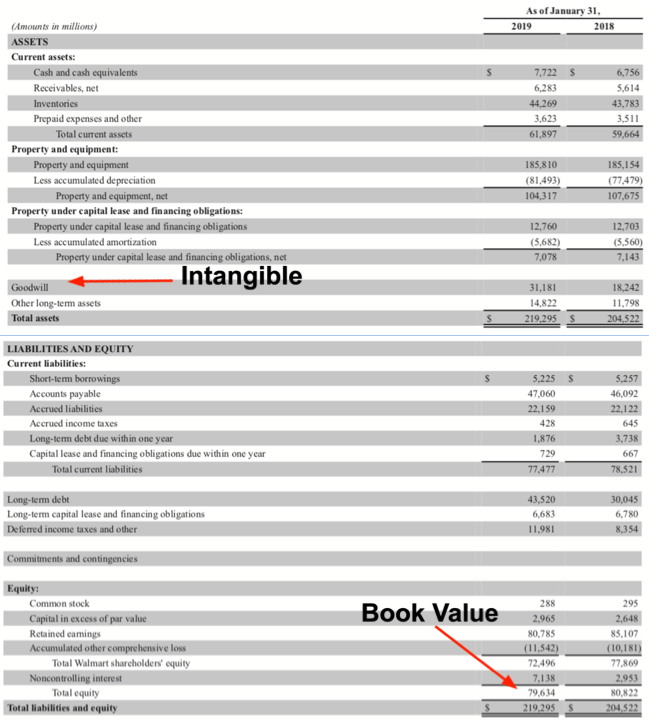

To get a better idea, let’s look at Walmart’s balance sheet:

Walmart’s BV as of January 31, 2019, was $79.634 billion. With 2.945 billion shares outstanding, Walmart’s BV per share would be $27.

Now, let’s say you could buy it for $17 a share.

As per BV measures, buying Walmart for $17 sure looks enticing.

Take a closer look at Walmart’s assets, though. Cash, receivables, inventory, and PP&E (property, plant, and equipment) all actually exist somewhere outside the balance sheet — they’re tangible.

But what about goodwill?

If Company A buys Company B, all assets and liabilities of the latter merge with the former at book value. But if Company A paid a price above BV for Company B, then that excess value goes to an account called goodwill.

In Walmart’s case, goodwill amounts to $31.181 billion.

If Walmart overpaid for its business acquisitions, then goodwill may end up being nothing but pumpkins and mice.

Bottom line is, goodwill doesn’t exist outside the balance sheet — it’s an intangible asset. This leads us to the value of tangible assets.

What is Net Tangible Assets Value?

Just as the name suggests, net tangible assets value (NTAV) is the value of a company’s tangible assets less all liabilities.

Walmart’s NTAV is $48.453 billion, or $16.5 per share, which means at $17 per share, it’d be only slightly above NTAV.

NTAV is just a more conservative measure of value than BV.

How Can You Spot Intangible Assets?

As I said before, tangible assets exist outside the balance sheet in the physical world, while intangible assets don’t. However, how can you spot intangibles?

Well, accounting standards usually require companies to explicitly tag intangibles on the balance sheet.

But, for clarity’s sake, here are some examples. Besides goodwill, intangibles could be software licenses, patents, or brands.

The value of brands is a bit hard to assess. If a company buys a brand, it has to carry it on the balance sheet at cost. But if the company develops its own brand, then it can’t record the brand as an asset.

That’s right. Coca-Cola didn’t buy its brand — the company built it, so you won’t find that intangible on its balance sheet.

Bottom line is, intangibles are very hard to assess.

Tangible asset values are more reliable. Walmart has $7.722 billion in cash, $6.283 billion in receivables, and $44.269 billion worth of inventory. The real values will not vary that much.

Net Tangible Assets Offer Above-Average Returns

NTAV is a more conservative valuation method than BV, and that’s important because stocks selling below NTAV offer investors higher returns than stocks selling below BV.

While academic research regarding NTAV returns is scarce, we can draw some conclusions from studies covering low price to BV stocks.

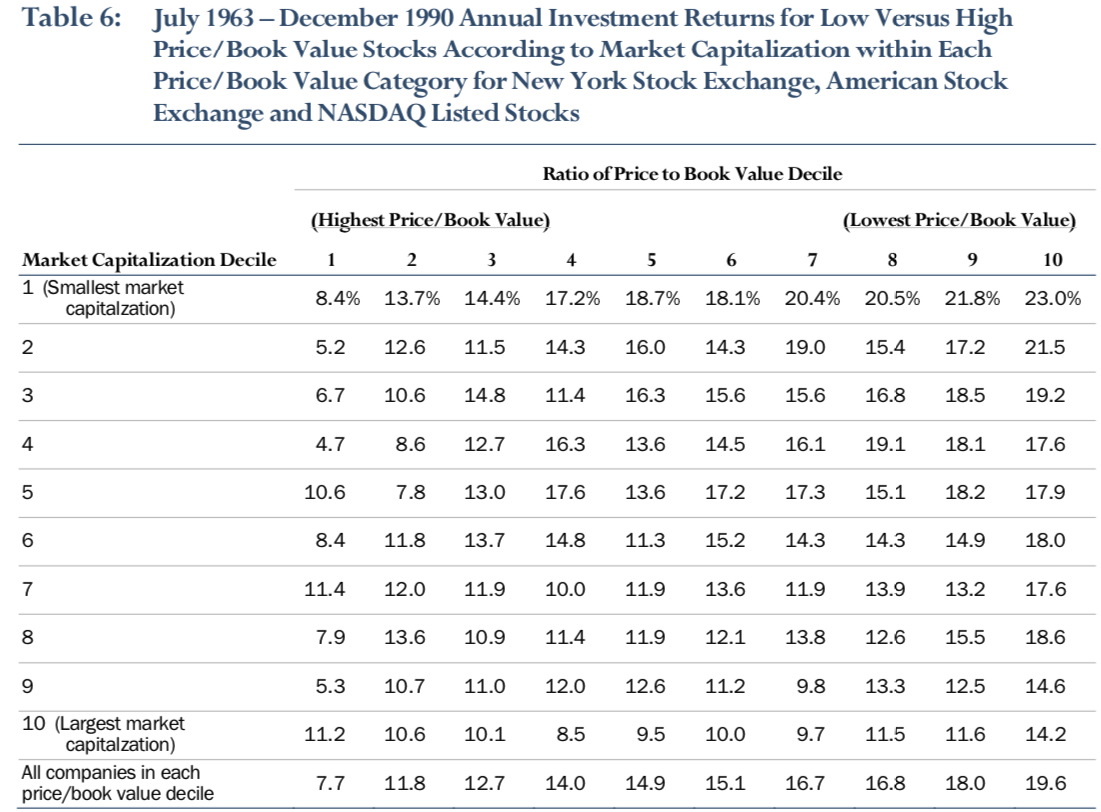

Eugene L. Fama and Kenneth R. French analyzed the returns of non-financial stocks in the NYSE, AMEX and NASDAQ indices.

They ranked stocks according to price to BV and market capitalization, and they got the following results:

The data shows that the smaller companies selling at the lowest prices in relation to BV offered the best returns — well in excess of the market average with a 23% annual rate.

Given that NTAV is a more conservative valuation metric than BV, we could extrapolate that among the cheapest stocks in relation to BV, there are also stocks with a low price to NTAV — for example, at a $100 BV and $70 NTAV, a stock selling for $35 has a 65% discount to BV and a 50% discount to NTAV.

But there’s more direct evidence.

The team at Broken Leg Investing ran some backtests and found that a group of stocks selling for less than 70% of BV had an 18.9% compounded annual growth rate (CAGR). But Broken Leg Investing also found that buying stocks with a 60% discount to NTAV returned a 27.5% CAGR during the same period!

Net Tangible Assets: The Superinvestors’ Choice

Superinvestors know buying cheap hard assets is a winning strategy.

Take Walter Schloss, who earned a 16% CAGR over a 40-year span, partly by focusing on net tangible assets.

For example, back in the ’80s, he bought Florida East Coast Industries, which had huge amounts of real estate in Florida. Or Clark Oil, a company with a bunch of gas stations he bought at $9 and sold for $27.

There’s also Peter Cundill. Throughout the ’70s, his fund returned an impressive 26%, while the stock market tanked.

His investment in Tiffany and Co. (Tiffany), the iconic jeweler and silversmith, reveals his preference for hard assets. He bought the stock at around $8, below a BV of $10.50. Tiffany held prime Manhattan real estate with a book value of only $1 million. It also had a factory of 120,000 square feet in Newark, New Jersey.

Also, Tiffany’s famous 128.5-carat diamond (the largest in the world) had a book value of only $1 — no zeros omitted — while its market value exceeded $2 million.

In less than a year, he sold his position at $19 per share.

Those are all impressive returns, but there’s an even more profitable investing strategy I’d like to discuss.

Net Tangible Assets: Why You Should Look for Net Nets Instead

While low price to BV is a solid strategy, and NTAV investing is superior given its more conservative approach, net nets are about as good as it gets for value investors focused on net assets.

Net nets are stocks selling for a price two-thirds below net current assets value (NCAV) — i.e., the value of current assets less all liabilities. This is a proxy for the liquidation value of a company.

If you could buy an operating company for less than its liquidation value — the most conservative valuation metric there is — then you’re probably getting a bargain.

Schloss said he turned to NTAV after he couldn’t find more stocks selling below NCAV on the US exchanges.

Cundill’s first criteria on his checklist read, “the share price must be less than book value. Preferably it will be less than net working capital less long-term debt.”

What are the expected returns with net nets?

Academic research shows that buying a group of net nets massively outperforms the market.

For example, Oppenheimer studied the performance of a basket of net nets over a 12-year period starting in 1970. Net nets trounced the market during that period with a 31% CAGR.

Joel Greenblatt, Richard Pzena and Bruce Newberg published a paper in 1981 concluding that a group of net nets returned a 40% CAGR for the period studied (1972 to 1978).

Graham said he averaged an annual 20% return investing on net nets for around 30 years. Warren Buffett also loved these dirt cheap stocks back when he ran his partnerships in the ’60s.

But, aren’t net nets an extinct species?

They’re scarce in the US stock market right now, but they’re alive and well in Japan, the UK, and other European markets.

They’re just usually too small for mutual funds managing large sums to take advantage of them — all the better for the small investor, since small companies offer better returns.

At Net Net Hunter each month, we comb through a list of around 1,000 net nets from around the world. Based on Graham’s selection criteria, we screen the raw list and send a monthly Shortlist to our members.

We save our members valuable hours of work so that they can focus on choosing from the best net nets available.

Members also have access to our Inner Circle Forum, where seasoned and amateur net net investors alike discuss investing strategies and stock picks.

If you want to learn more about net nets and begin profiting from this solid investing strategy, join us now.

Start putting together your high quality, high potential, net net stock strategy. Click here to get free net net stock checklist.

Article image (Creative Commons) by theilr, edited by Net Net Hunter.