Your Essential Guide to Net Net Stocks

In 2014, Warren Buffett explained that the net nets he bought in the 1950s helped him achieve the highest returns of his career. Evan has used lessons from Warren Buffett, Benjamin Graham, plus other top investors and academic studies to select stocks for his own portfolio and make those stock available on Net Net Hunter’s VIP Newsletter. Get full access to our VIP Newsletter right now, for FREE. Click Here.

Net net stocks can be fabulous investments, but what exactly are they?

And, how can investors take advantage of this classic investment strategy?

Unfortunately for my portfolio, it took me a long time to transition to Graham's net net stock strategy. As I explained to Alvin Chow of Dr Wealth, a number of half-baked articles critical of Graham's favourite investment strategy convinced me that net net stocks didn't exist anymore. As a result, I mistakenly bought into the widespread belief that net net stock investing wasn't a viable strategy. Value investors need to ignore the financial media.

Boy was I wrong. Since diving head-first into the investment strategy in 2010, my portfolio has really taken off. In fact, Graham's net nets have worked so well that my portfolio has blown past the market's return since making the switch.

More on that in a bit. Here's what you can expect in this essential net net stock guide:

What Exactly Is a Net Net Stock?

Essentially a net net stock is a low Price to Book stock but where the “B” in the P/B ratio has been stripped of all long-term assets. That's about the easiest way to explain the concept.

Why strip away long term assets?

Stripping away long term assets turns book value into what net net stock investors call net current asset value (NCAV). By focusing only on the NCAV of the company, a net net stock investor is calculating a highly conservative estimate of the company’s liquidation value.

When developing the investment strategy in the 1930s, Benjamin Graham found that a company's net current asset value was a good proxy for a firm's real world liquidation value. Often 3rd party acquisitions of the entire company were made for a price roughly equal to the firm's NCAV and wholesale liquidations of a company resulted in shareholders receiving an amount equal to the company's NCAV per share. What impairment in value a firm's current assets saw was often made up by the value of the company's long term assets which were excluded from the original calculation.

Calculating a firm's NCAV is really straightforward:

Current Assets

Less Total Liabilities (Including Off Balance Sheet Liabilities)

Less Preferred Shares

NCAV

Market Capitalization / NCAV

Price to NCAV

The lower the ratio the cheaper the stock. If the Market Capitalization of the company is $50 Million and the firm's NCAV $100 Million, for example, the company is much cheaper than if it had a Market Cap of $75 Million. In the first scenario the firm is trading at a 50% discount to NCAV while in the second it's trading at a tiny 25% discount. As I'll talk about below, this is a crucial difference.

Often a firm can shrink or increase its NCAV by buying back or issuing common shares. This can distort how stable a firm's asset value appears, so I like to place NCAV on a per share basis:

Price Per Common Share / NCAV Per Common Share

Price to NCAV of the investment.

Doing this provides an investor with a much more relevant assessment of the firm's NCAV because it accounts for the shift in shares outstanding. If your assessing a firm's NCAV stability a shrinking share count can make the firm's NCAV seem much less resilient than it actually is.

When it comes to net nets, there are a few different names to remember. I've talked a lot about a firm's NCAV, so it should be no surprise that another name for net net stocks are NCAV stocks. Warren Buffett talks a lot about "Cigar Butts," when referring to net nets, and Graham often called these sort of investments "Working Capital" or "Net Working Capital" stocks. Buffett's term, cigar butts, referred to how unappetizing yet profitable these stocks are. While not the sort of companies you'd want to hold onto for the long term, they're selling so cheaply relative to value that buying them is akin to finding a nearly finished cigar on the sidewalk. It costs nothing to pick up so those last couple of puffs are pure profit.

“The many dozens of free puffs I obtained in the 1950s made that decade by far the best of my life for both relative and absolute investment performance.” – Warren Buffett

You may also hear the term NNWC, or Net Net Working Capital stocks. These are essentially net nets but where the current assets have been further discounted before subtracting all liabilities, preferred shares, and off balance sheet liabilities. Doing this allows an investor to arrive at the NNWC figure of the company.

Discounts can vary, but roughly equate to:

Cash and Equivalents @ 100%

Short Term Investments @ 90%

Receivables @ 75%

Inventory @ 50%

Prepaid expenses @ 25%

Deferred Tax Assets @ 0%

Should you discount current accounts or not?

I don't. A properly discounted net net stock will perform just as well as a NNWC stock, on average. Click Here to learn more.

As you might have guessed, the extremely conservative appraisal of liquidation value is one reason these stocks do so well. Generally, the cheaper you buy a stock at the better your return is going to be. Using a conservative estimate of the company’s value keeps a value investor from buying stocks at too thin of a spread between price and value. In the end, a net net stock investor is buying a fantastically cheap investment.

Why Are Net Net Stocks So Cheap?

And for good reason. Companies with Market Caps below their NCAV are often very troubled – they’re facing large business problems that investors just don’t think the company can come back from. Sometimes these problems reach to the core of the business, such as a major industry disruption that has all but killed a company’s only product.

It's not uncommon to find companies that have seen their revenue decimated by as much as 90%, and their earnings turn to large losses. If you see a company devastated this way, the last thing you want to do is buy stock in the company. In fact, if a typical investor owns shares in the company, he's very likely to want to dump the investment.

That reaction is understandable. In situations like that, investors have little hope that the company will survive, especially if the firm has debt to pay off. But, not all distressed situations are created equally. Some distressed firms are stuffed with current assets and have little in the way of debt or liabilities. It's these companies that astute value investors swarm in to buy.

The key fact to remember is that Graham's net net stock strategy is focused on assets, not earnings, and specifically current assets. Many firms that have quickly eroding operations still have current assets that remain resilient. If the stock is priced low enough relative to the firm's net current assets, it may constitute a net net stock and be an outstanding buy candidate. In the end, it doesn’t matter if the company continues operations or not since there are a number of ways that the investment can turn out really well.

Three Common Ways to Win Big

I want to point out right here that Graham favoured net nets that had positive earnings and were paying a dividend. Having said that, the evidence from academic and industry white papers show that positive earnings aren't really important when it comes to buying net nets and dividends can actually reduce returns. This is partly due to how investors tend to profit by buying net nets.

I’ve found that there are four common ways value investors make money from net net stocks: liquidation, 3rd party buyout, price spike due to good news, and recovery in operations.

Obviously, if the company doesn’t have a hope of continuing its business then liquidation is a real possibility. Since net net stocks are purchased so cheap, though, liquidations can ultimately mean a quick cash windfall. In these situations, the company distributes the cash received for the assets directly to shareholders. In a full liquidation scenario, the firm will have to cover its liabilities before distributing anything to shareholders.

A firm can also partly liquidate, selling the assets asociated with a money-losing division and then distributing that cash to shareholders. Ironically, while Graham's strategy is based on liquidation value, firms rarely liquidate.

To be completely honest with you, I’ve never owned a firm that's decided to liquidate. If you hold a portfolio of well-chosen low Price to NCAV stocks, then it’s much more common for your company to be scooped up by another, larger, financially healthy company. In fact, this has happened with roughly 20% of my net net stocks. Usually the troubled company has some asset – some brand, piece of real estate, or market position – that another company covets. Since the price of the company’s stock is so low, making an offer to buy the entire company becomes very enticing.

These buys usually take place around a company's NCAV, which I find really interesting. This is inline with the comments Graham had about net net stock buyouts years earlier. In fact, Benjamin Graham summed up his thoughts on net net investing and final recommendation in his last ever interview - it's well worth a read.

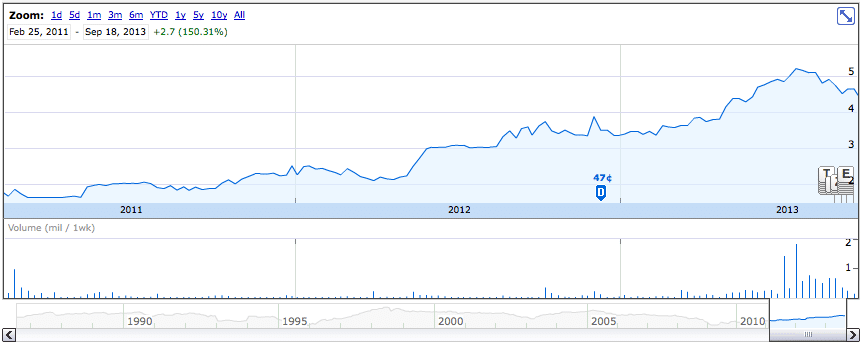

Also interesting is the behaviour of net nets when a bit of good news comes out about the company. In these situations, a depressed stock can rocket up in price well past NCAV. These events are probably due to the powerfully negative sentiment attached to net net stocks. Often a company's stock price is so depressed and so illiquid that when a bit of good news comes out, people realize their mistake and rush in to buy (or cover their short), sending the share price skyrocketing. Just take a look at what happened to InfoSonics:

In fact, I liked the investment so much that I bought it a second time in 2013. Bizarrely, the exact same thing happened again:

At the far right side of each chart you can see the stock price leap roughly 100% due to a bit of good news. With prices this low, and an outlook this gloomy, it doesn’t take much good news for a company’s stock to rocket up 50 or even 100% in value. This is fairly common, but just one of 4 ways net net stocks work out.

The remainder of the companies usually miraculously fix their operations which sends their stocks soaring. Buffett says that turnarounds seldom turn, but when it comes to net nets companies improve their operations at least 1/3rd to 1/2 of the time. Twinbird was one of these amazing investments. And, take a look at one of my favourite stocks of all time, Trans World Entertainment:

In the case of Trans World Entertainment, I made just under 200% in 27 months, for an 89% annualized return. I got in late, however. The company's operations had been improving since 2009. If an investor had of picked up the stock and held on until the stock price reached its NCAV Per Share, it would have been possible to make 600 to 700% on the investment. Outstanding!

Returns On Offer to Net Net Stock Investors

When I started investing, I had no idea that you could buy 10-Baggers using the strategy. While Trans World Entertainment is certainly impressive, take a look at Voltari Corp, which shot up in price in 2015. Voltari was a 24-Bagger.

I want to say right here that, while it does happen, it's not that common to find a 10-bagger in your portfolio and 20-Baggers are even rarer. Whether you could have netted a 2000% return with Voltari Corp really would have come down to when you managed to sell, and that would have depended on what sort of sell strategy you put in place. One of our members set his sell strategy at selling either after a 1 year holding period or after a 1000% increase, whichever comes first. That won't net him a 2000% return, but it could net him a 1000% return if he is lucky enough to select another 10-Bagger.

So, what sort of returns can a typical net net stock investor expect?

If you are selecting decent net net stocks (ie. if you're excluding Chinese firms, resource exploration companies, and other industries not conducive to great net net stock returns), I think it's perfectly reasonable to expect a return 15% above the overall market return. Since the American markets have returned roughly 10% over the long term, that would equate to cumulative average returns of 25%+.

Sound far fetched?

I agree. It does. After all, even top money managers don't achieve those kind of returns. But, I have good reason to think that those sort of returns are perfectly achievable. If you want to get an idea of what sort of returns you can expect from these sorts of stocks, you really have to look at academic and industry studies. And, what better place to do so than in an essential net net stock guide? Here goes...

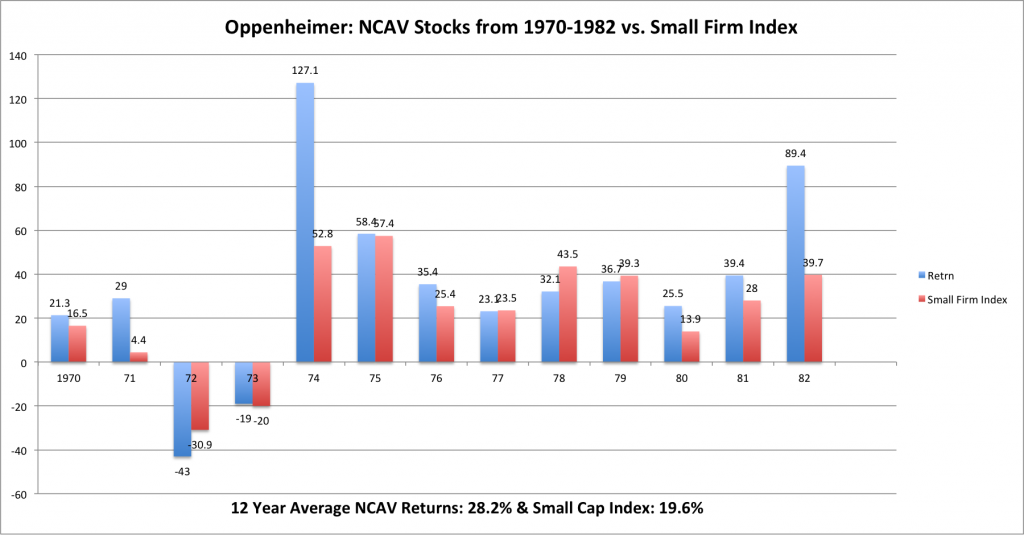

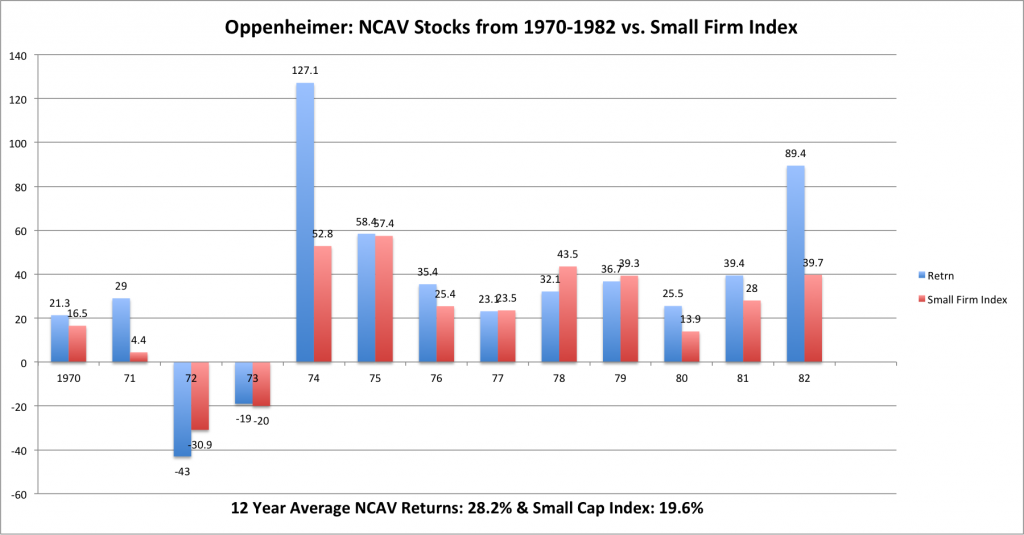

Ben Graham's Net Current Asset Values: A Performance Update, by Oppenhiemer

No, he's not the same man who built the bomb.

Oppenhiemer did write one of the most famous papers on Graham's net net stocks, however.

The study spanned 12 years and two recessions. Let's look:

In Oppenheimer's study, $1 invested at the start of 1970 would have became...

Net Nets: $25.92

Small Firm Index: $10.20

...in 12 years. That's a CAGR of over 31%!

Looking at the bar graph, net net stocks were also able to beat the market in 9 out of 13 years, or 69% of the time. That was more than enough to offer over twice the investment return of the S&P 500.

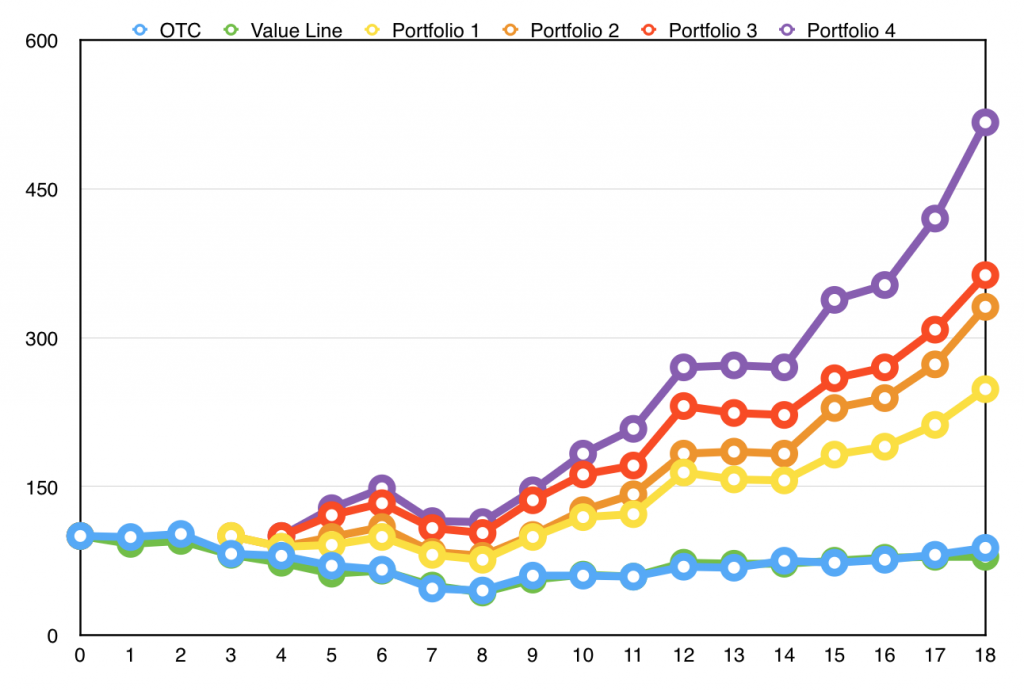

How the Small Investor Can Beat the Market, by Greenblatt, Pzena, and Newberg

I've written a detailed article about this study which you can read on Net Net Hunter. Click here.

Greenblatt and friends studied the performance of 4 portfolios from April 1972 to April 1978.

Portfolio 1

Price below NCAV

PE floating with corporate bond yields

No dividends required

Portfolio 2

Price below 85% of NCAV

PE floating with corporate bond yields

No dividends required

Portfolio 3

Price below NCAV

PE of less than 5x

No dividends required

Portfolio 4

Price below 85% of NCAV

PE of less than 5x

No dividends required

As expected, net nets dominated the market.

Graham's Net-Nets Outdated or Outstanding, by James Montier

Montier is an active proponent of mechanical investing, net nets being one mechanical investment strategy. He's also a solid Grahamite, favouring old school value investing along with folks like Tweedy, Browne and Walter Schloss.

In a paper he wrote for GMO, he studied the returns of Japanese net net stocks from 1985 to 2007. In fact, I wrote about that study here. The period of study includes the 1989 Japanese market peak, and sizeable decline in the Japanese stock market over the following 18 years.

Not surprisingly, Japanese stocks disappointed over the period, returning a CAGR of just 5%. Net net stocks trumped the market, though, netting a 20% CAGR! That return compared nicely to European and American net nets over the same time period.

Ben Graham's Net Nets: Seventy-Five Years Old and Outperforming, by Carlisle, Mohanty, & Oxman

Carlisle (yes, the same Carlisle of Greenbackd fame), Mohanty, and Oxman looked at the returns of net net stocks from 1983 to 2008, a period of 25 years. They then compared those returns against NYSE-AMEX and Small-Firm indices.

Returns were outstanding. Net net stocks recorded an average monthly return of 2.55%. That showing was good enough to beat the NYSE-AMEX return by 22.42% per year. That's an excess return of 22.42%.

Net nets also beat the Small-Firm index by 16.9% per year -- again, that's nearly a 17% outperformance over the small stock index.

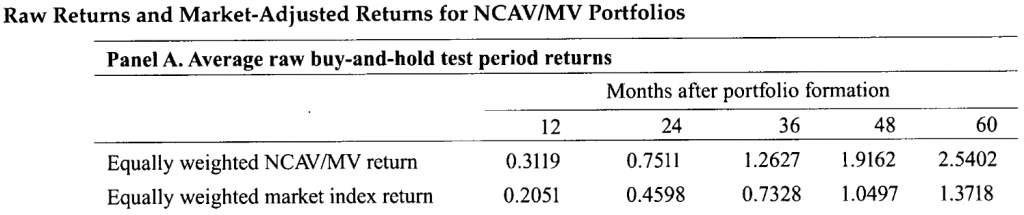

Testing Benjamin Graham's Net Current Asset Value Strategy in London, by Xiao & Arnold

Xiao and Arnold looked at net net stocks in London from 1980 to 2005. Returns were calculated over 12, 24, 36, 48, and 60 month periods.

As you can see, the returns for net net stocks were very good. Net nets provided tremendous outperformance over all periods. In this study, the average 12 month return to a basket of net net stocks was 31%! The FTSE 100, obviously, didn't come anywhere close to that return.

These are just some of the studies that are available which cover net net stocks, but everything I've read has shown similar performance. Since I started in depth research of Graham's net net stock strategy in 2010, I have not yet come across a study that shows that properly discounted net net stocks don't vastly outperform the American markets. If you have a study that shows that, please email me at support [at] netnethunter.com.

One last thing I want to point out as far as net net stock returns go is that depending on the net nets that you pick, such as growing or shrinking NCAV, you could either do substantially better or worse than average. If you insist on sticking with American net nets, you'll inevitably be faced with a large number of Chinese reverse merger scams. Buying these sorts of stocks will ultimately lead to lower returns given the extreme fraud risk. On the other hand, investing internationally will give you the chance to buy Greenblatt-like net nets, outperforming net net stocks in general by a wide margin. As shown above, Greenblatt's net nets beat the OTC Market by roughly 30% per year. To read about this study, click here.

These are the sort of net nets that I like to invest in. As I mentioned before, my own record with net nets has been very good. You can read about my early investment returns here, before I switched to Interactive Brokers. Over the previous two years my returns have come down a bit mostly due to the fairly flat year we had in 2015 and due to being partly out of the market (a costly mistake on my part).

Common Pitfalls of Net Net Stock Investing

So, what's the catch?

If the strategy works this well, then there must be some catch. If not, everyone would pile into these stocks, destroying the ability for people like you and me to profit from the strategy.

One catch is that this strategy doesn't work all of the time. That's both a good and bad thing for small investors. Tweedy Browne claims that even the best professional investors have long periods of underperformance. At least, that's what they showed in this study.

Small investors make the mistake of thinking that just because the strategy didn't work over a year's time when they used it, the strategy doesn't work at all. This is known as short-termism or "what you see is all there is" (WYSIATI). Extending your line of sight ten years allows you to see the beauty of this strategy and stick with the strategy long enough to reap the rewards on offer.

Take another look at the returns in Oppenhiemer's study:

What would have happened if you began investing in net nets in 1972 and then pulled out of the strategy due to the terrible results? You would have missed the eventual 127% and 58% return seen in 1974 and 1975. If you stuck around after those first terrible two years, you would have been up 66% over the 4 year period versus the market's 33% rise.

Likewise, what if you abandoned the strategy after 3 years of market underperformance from 1977 to 1979? You would have missed the outstanding returns from 1980 to 1982. If you were one of the more thoughtful investors and hung on during that period, however your returns would have been 637% versus the market's 403% return ...over 6 years.

Graham's net net stock strategy doesn't beat the market every year– and it's a major mistake to think otherwise. There will be some years of underperformance, many years of outperformance, and even some money-losing years. All of these years factor into the returns of net net stocks over the long term.

Often investors attempt to avoid these market drops by timing the market. While I'd love to be able to avoid large market drops and only buy before large advances, thinking that that's a viable strategy is nothing more than fantasy. Being out of the market means lower long term returns, so it's better to just ride the ups and downs of the market.

Another WYSIATI trap is the failure to diversify and then abandoning the strategy when the one or two stocks you picked didn't work out as you expected them to. This is nutty. Whenever you invest in net nets you are buying into troubled deep value situations and some of these investments ultimately won't work out. According to Buffett, roughly 70 to 80% of your net net stocks will work out. The others will disappoint.

It's also pretty obvious that each of your stocks won't return an identical, say, 25% per year to achieve that great portfolio return. In reality, some will produce higher returns and some will return less than the group average. If you only buy a couple of stocks, you'll end up with returns that fall anywhere along a long spectrum of possibility. In fact, there is a pretty good chance that the one or two stocks you'll pick will underperform the average returns seen by long term net net stock investors.

Of course, professional investors are well aware of all of this, so you would expect that they would pile into the investment strategy to reap the great returns on offer. Fortunately for people like you and me, net net stocks only exist among the micro and nano cap spectrum. They also tend to be thinly traded, so very illiquid. This means that professional managers just can't buy these sorts of stocks. In fact, they're mostly forced to buy companies above $1 Billion in Market Cap. That's far from net net territory, typically below $100 Million in Market Cap.

Ironically, most small investors make the mistake of forfeiting their structural advantage (investing small sums of money) in favour of buying large cap companies along side the pros. That's insane. They're also turned off by companies facing business problems, preferring instead to buy late Buffett-styled firms with moats. I call this error, assuming you can do what Warren Buffett does, "The Warren Buffett Trap".

Finally, a lot of investors new to net net stocks select firms that have terrible odds of producing great returns. Stocks that net net rookies often buy are Chinese reverse merger scams, net nets loaded with debt, or even resource exploration firms. None of these companies make for good net net stocks.

Narrow Focus Vs. Broad Focus in NCAV Investing

The discussion above should make one thing fairly clear: investors should really take a broad focus rather than a narrow focus on their investing when it comes to net net stocks.

Investors have to make two mental shifts before they start investing in net net stocks. Focusing on the Balance Sheet over the Income Statement is the first shift, and adopting a broad view of investing is the second.

A narrow focus refers to performance over a short time horizon or focusing on the success or failure of individual stocks. Most value investors focus a lot of attention on what an individual company will do going forward and focus far less attention on how their portfolio is constructed. They end up putting a lot of time and effort into conducting in depth research on individual stocks in an attempt to forecast the future.

Net net stock investors, on the other hand, focus on a few telling characteristics of a company and almost totally ignore qualitative research. This is because net net stock investors know that they are using a mechanical investment strategy and that the success of their portfolio depends on the statistical return characteristics of net nets in general. Net nets as a group have yielded roughly 15% over the market return since the 1930s so, as long as they have selected their net net stocks intelligently, they should see a very similar return on average over their lifetime.

Taking a broad perspective and leveraging the returns associated with net net stocks in general takes a good amount of diversification. How much? The more the better. If you're randomly selecting net net stocks then, according to my university statistics professor, 30 stocks is when your portfolio would start to approximate the population of net net stocks. Graham bought 100s of net nets, but I'm after the highest possible returns.

That means that whenever I buy net nets, I try to buy the highest quality picks. These are stocks that have growing NCAV, growing earnings, no debt, tiny Market Caps, are trading at 50% of NCAV or less, and have PEs of 10x or less. These sort of stocks are as rare as they are profitable. If I can find enough of these companies, then I'd be comfortable holding ten stocks. The further away from this ideal that the stocks available get, the more diversification I demand. I recommend that Net Net Hunter members buy 10 to 20 net net stocks, and never buy average quality net nets. Doing so should drastically increase the returns achieved and help prevent investors from buying into frauds.

How to Get Started

If you want to get started in net net stock investing, you should definitely educate yourself as much as possible before making an investment decision.

Unfortunately, there aren't many good books available on net net stocks. Tobias Carlisle of the well respected website Greenbackd.com has a great book out called Deep Value, which is worth a read. While Tobias definitely knows his stuff when it comes to deep value investing, the book may not go into as much detail on net net stocks as you may like. Bruce Greenwald's Value Investing: From Graham to Buffett and Beyond also touches on net nets, but only briefly.

To be honest with you, I've had to learn much of this stuff myself through my own research and piecing facts and figures together from a broad range of sources. There just isn't much good quality information available. Trying to find reputable sources has been a very challenging and frustrating experience. Doing so has forced me to go back to high quality original research available in university databases. That's why I put together my own net net stock guide, Retire Young & Rich.

As most of our members know, I put this website together to solve my own problem, not being able to find enough high quality net net stocks in the US. To justify the large cost and enormous amount of work involved, I decided to open my work up to like-minded investors. Part of this process involved writing my own investment guide for people who want to learn more about net net stocks and how I select them. That's how Retire Young & Rich came about.

Another option open to you is joining our mailing list. Every week I send out detailed information about investing in net net stocks, and a high quality net net stock pick at the end of each month. If you want to get into net net stock investing, this the easiest step you could take.

The best step, on the other hand, would be joining our community. Every day I spend a good amount of time talking to our members about net net stocks, answering questions, and helping members put together good quality net net stock portfolios to achieve their investment objectives. By joining Net Net Hunter, you get direct access to me and all of the information I've gathered on how to invest using Graham's favourite strategy. You also get high quality stock research, shortlists of the best net net stock opportunities, access to our Inner Circle Community Forum, Inner Circle Advice emails, our Inner Circle Newsletter, our Inner Circle Resource Center, and 1-on-1 help implementing the strategy. Really, if you're interested in becoming a net net stock investor, there's no better place to learn. Get more information on joining Net Net Hunter. Click Here right now.

Your Essential Guide to How I Select Net Net Stocks

The second best sources of in depth information on net net stocks is my net net stock guide, Retire Young & Rich. Click on the link below for more information.