Warren Buffett’s Cheap Stock Picks and Investment Strategy

Download these original articles in How To Choose Deep Value Stocks Like A Young Warren Buffett for FREE right now. Click Here.

Warren Buffett likes cheap stock picks. Hunting for bargains is his thing. He just can’t help it.

I know you might be thinking, “This guy doesn’t know what he’s talking about. Isn’t Warren Buffett the one who said it is better to buy a wonderful business at a fair price than a fair business at a wonderful price?”

That’s true. It’s one of the reasons most people think of Buffett as a moat investor. But at heart, I’d say Warren Buffett is still the 20-something kid who loves cheap stocks. In fact, many of Buffett’s cheap stock picks over the last 20 years show a nostalgia for the sort of stocks he bought in the ’50s and ’60s.

Why wouldn’t he? After all, he owes his most impressive returns to these cheap stock picks.

That’s right, while running his Buffett Partnerships back in the ’50s, he returned an impressive 24.5% compounded annual rate to his partners — 29.5% before fees. Berkshire Hathaway had a 20.5% compounded annual growth in market value since 1965 — the year Buffett became its CEO.

Back in the ’50s and ’60s, Buffett focused on deep value stocks — i.e. very depressed stocks selling at prices below liquidation value or even book value.

He measured value, then, in quantitative terms. However, if these deep value stocks also had attractive qualitative features — like growing earnings, excellent management, or a competitive advantage — he’d like them even more. He just didn’t like to pay for quality per se.

It was only at Berkshire Hathaway that he had to start paying for quality and moats, even without a discount to asset values.

Why did he change his strategy?

It was a matter of size. Deep value investing only works with small sums, and Berkshire Hathaway was very big compared to Buffett’s partnerships.

Over the last 20 years, though, Buffett bought deep value stocks for his personal portfolio — he found them in the Korean stock market. Finding this group of cheap stock picks, Warren Buffett says, was “like finding a new girl to me.”

As you’ll see throughout this article, if you’re working with small sums you have an edge. I’ll give you a hint what that edge is — fund managers and institutional investors can’t match your size.

But you need Buffett’s early investment strategy to exploit that advantage. Dissecting some of Warren Buffett’s early cheap stock picks will help you get a very good idea of what to look for in stocks for your deep value portfolio.

The Law of Diminishing Returns and the Small Private Investor’s Edge

Why do small private investors have an edge?

On June 23, 1999, in Business Week, Buffett said:

“If I was running $1 million today, or $10 million for that matter, I’d be fully invested. Anyone who says that size does not hurt investment performance is selling. The highest rates of return I’ve ever achieved were in the 1950s. I killed the Dow. You ought to see the numbers. But I was investing peanuts then. It’s a huge structural advantage not to have a lot of money. I think I could make you 50% a year on $1 million. No, I know I could. I guarantee that.”

So, Buffett believes that smaller sums can expect higher rates of return than bigger sums.

In economics, that’s called the law of diminishing returns.

In 1999, at Berkshire’s annual shareholders meeting, when asked if there were opportunities in the stock market for the small investor, Buffett remarked:

“I think, working with a very small sum, that there is an opportunity to earn very high returns. But that advantage disappears very rapidly as the money compounds. Because I, you know, from a million to 10 million, I would say it would fall off dramatically, in terms of the expectable rate.

Because there are little — you find very small things that, you know, you can make — you are almost certain to make high returns on. But you don’t find very big things in that category today.”

So, Buffett believes small private investors have an edge.

Exactly why is that?

For regulatory concerns, institutional investors don’t like to own more than 10% of any company’s shares outstanding, and they hold at least 20 to 30 stocks at any given time.

The average mutual fund has $1 billion assets under management. This means they have to look for companies worth $200 to $400 million.

For the same reason, funds managing $20 billion are limited to investments in companies with market caps around $2 billion or more.

There are only around 400 companies with market caps of $4 billion or greater.

True, a $1 billion fund has nearly 5 000 stocks to choose from, but there are nearly 14 000 mutual funds — nearly three mutual funds for every stock!

This area of the stock market is crowded and, thus, highly efficient. Discrepancies between price and value are small and quickly erased. The small private investor is clearly at a disadvantage in this playing field.

However, in the universe of stocks with market caps below $100 million, the small private investor faces almost no competition from professional money managers. Fund managers just can’t waste their resources analyzing tiny stocks.

This is, then, a highly inefficient corner of the stock market, where discrepancies between price and value are usually very large.

High discrepancies between price and value can turn into abnormally high returns, and that’s why the small private investor has an edge.

Small sums are, indeed, a structural advantage.

What is a small sum, though?

Between a few thousand and ten million dollars, I’d say — some would argue you can go as far as fifty million.

If you’re in that range, you’ll definitely want to read the next chapters to discover how Warren Buffett cheap stock picks’ strategy can be applied today.

Focus on the Group Outcome

To get an idea of how Buffett would invest small sums today, we should look at what he did when he was working with small sums, back in the ’50s and ’60s.

Let’s take a look at his early investment strategy first. Then we’ll focus on specific cheap stock picks.

Buffett Partnerships’ portfolios had at least three kinds of investments.

The first kind were deep value stocks — these were Warren Buffett’s cheap stock picks. He called them “generals” then — and later on, he’d call them “cigar butts."

He would have around 80% of the portfolio invested in generals — with some diversification for sure, but clearly concentrated on his best ideas.

In his words, “we usually have fairly large positions (5% to 10% of our total assets) in each of five or six generals, with smaller positions in another ten or fifteen.” (Buffett Partnership Letter, 1963)

These generals usually had prices below net current asset value (NCAV), or eventually, below tangible book value (BV).

The second largest part of the portfolio consisted of “workouts." These were basically arbitrage situations arising from mergers, liquidations, reorganizations, and spin-offs.

Workouts led to almost sure profits, which were also limited.

Then Buffett would have “control” situations in which he took control of the company to influence its policies and decisions to unleash value.

Let’s focus on the first category.

Buffett knew, from Benjamin Graham’s teachings, that a basket of deeply undervalued stocks — i.e. mostly low price to NCAV, but also low price to BV, and low PE stocks — almost certainly outperformed the market in the long run.

Graham called investing in a basket of net nets — i.e., a group of 20 or 30 stocks at prices below one-third of NCAV — a “foolproof” method to beat the market. He made around 20% annually investing in net nets for almost three decades.

That’s why Buffett invested in net nets heavily, concentrating in a select few and keeping the rest of his portfolio in a group of around 20.

Like Alice Schroedinger mentions in her book, The Snowball: Warren Buffett and the Business of Life, while running the partnerships, he followed Graham’s principles to the letter, “everything he bought was extraordinarily cheap, cigar butts all, soggy stogies containing one free puff.”

Smart stock selection was the key to his superior result, though.

Considered individually, most of these generals looked like terrible investments.

There was something wrong about the business, the management, or both. But the price was so low — as I said, most had prices below NCAV — that even in a worst-case scenario, the investor would earn something.

Buying these stocks was like picking up cigar butts from the street and smoking the last free puff. All the profit was free, but there was something disgusting about it.

But, the focus was on the group outcome. Even with the very cheap price, you wouldn’t like to have all of your net worth in one of these cigar butts. You needed a group of them (around 20 or 30) for the strategy to actually work.

If only 60% of these investments actually worked out, you’d have a decent outcome of around 20% compounded annually, according to Graham, Buffett, and Walter Schloss, to give you some examples.

Let’s look at Warren Buffett’s cheap stock picks in detail.

Warren Buffett’s Cheap Stock Picks: Western Insurance Securities

Buffett used to write a column called “The Security I Like Best” for The Commercial and Financial Chronicle in the ’50s, where he discussed his best ideas.

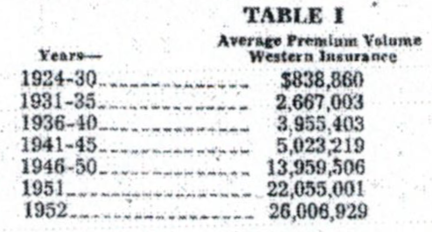

On April 9, 1953, Buffett discussed his investment in Western Insurance Securities, calling it “a young, rapidly growing and ably managed insurance company."

It operated through two subsidiaries, Western Casualty & Surety and Western Fire.

With a premium volume of $26,009,929 and consolidated assets of $29,590,142 in 1952, it was also a growth stock (see image below).

It had great management in place — according to Buffett —, but the best thing about this stock was its price of less than 2 times earnings and a discount to BV of around 55%. While technically not a net net, it traded well below liquidation value.

This stock was a mix of deep value with qualitative features.

Warren Buffett’s Cheap Stock Picks: Sanborn Map Co.

Sanborn Map Co. (Sanborn) was a company specialized in the continuous publication and revision of detailed maps of all the cities of the United States.

Its primary customers were fire insurance companies. For 75 years, it was more or less a monopoly, but insurance companies placed directors on Sanborn’s board to supervise its actions, as they were its biggest clients.

During the ’30s, Sanborn invested its retained earnings in securities, about half in bonds and half in stocks.

In the ’50s, the map business shrank as fire insurance companies didn’t need maps as they did before, but Sanborn’s investment portfolio soared. At the same time, its stock price sank.

Maybe Buffett can explain that better:

“Let me give you some idea of the extreme divergence of these two factors. In 1938 when the Dow-Jones Industrial Average was in the 100-120 range, Sanborn sold at $110 per share. In 1958 with the Average in the 550 area, Sanborn sold at $45 per share. Yet during that same period, the value of the Sanborn investment portfolio increased from about $20 per share to $65 per share. This means, in effect, that the buyer of Sanborn stock in 1938 was placing a positive valuation of $90 per share on the map business ($110 less the $20 value of the investments unrelated to the map business) in a year of depressed business and stock market conditions. In the tremendously more vigorous climate of 1958, the same map business was evaluated at minus $20 with the buyer of the stock unwilling to pay more than 70 cents on the dollar for the investment portfolio with the map business thrown for nothing.” (Buffett Partnership Letter, 1961).

Buffett put about 35% of his partnerships’ assets in Sanborn, and acquired control of the company.

Sanborn was a net net, with no particular business quality or growth prospects, but acquiring control of the company gave Buffett the ability to uncover value, at a very decent profit.

Another classic Warren Buffett cheap stock pick — a true bargain.

Warren Buffett’s Cheap Stock Picks: Dempster Mill Manufacturing Company

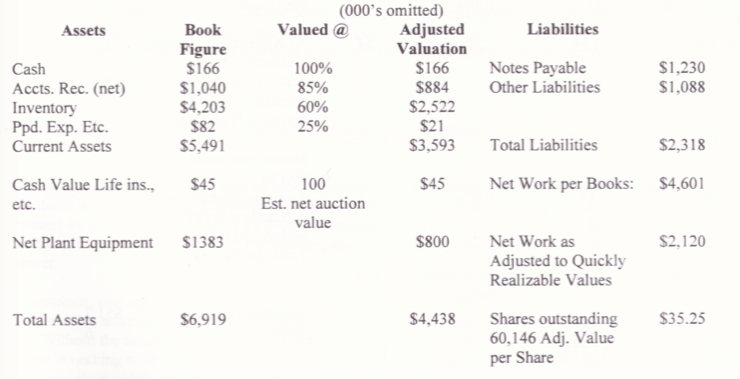

Buffett also acquired control of Dempster Mill Manufacturing Company (Dempster Mill) in 1961.

He assessed the value of Dempster Mill “on the basis of what I thought a prompt sale would produce at that date" — i.e. its liquidation value.

In his 1962 letter, he let his partners see how he valued the company (see image below).

This is what we would call a net net working capital (NNWC) valuation. You take the value of current assets, adjust it by a conservative measure, then subtract total liabilities.

Dempster Mill’s NNWC as of December 1961 was $35, and Buffett bought for an average price of $28 per share.

Keep in mind that’s a 20% discount to an ultra-conservative valuation metric.

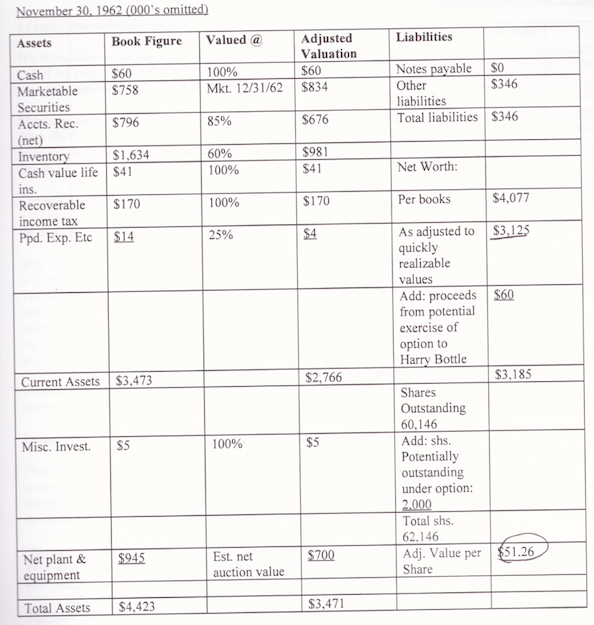

By the end of 1962, after about a year under Buffett’s direction, Dempster Mill’s NNWC was $51 (see image below).

By increasing the efficiency of the company and investing the resulting cash in a securities portfolio — we can assume it was a deep value portfolio — Buffett managed to increase the value of his holding by 45% in one year.

Referring to this situation, in his letter to partners that year, he said:

“…by buying assets at a bargain price, we don’t need to pull any rabbits out of a hat to get extremely good percentage gains. This is the cornerstone of our investment philosophy: Never count on making a good sale. Have the purchase price be so attractive that even a mediocre sale gives good results. The better sales will be the frosting on the cake."

The frosting of the cake came the following year, when he sold Dempster Mill at $80 per share for a total gain of around 185%.

In his January 1964 letter to partners, Buffett reflected on his investment strategy, while referring to Dempster Mill:

“The situation started as a general in 1956. At that time, the stock was selling at $18 with about $72 in book value of which $50 per share was in current assets (cash, receivables and inventory) less all liabilities. Dempster had earned good money in the past but was only breaking even currently.”

There was nothing enticing about Dempster Mill’s business. It was just too cheap — selling at $18 with a NCAV of 50.

Buffett’s focus was on the group outcome, though. Referring to Dempster Mill, again, he wrote:

“The qualitative situation was on the negative side (a fairly tough industry and unimpressive management), but the figures were extremely attractive. Experience shows you can buy 100 situations like this and have perhaps 70 or 80 work out to reasonable profits in one to three years. Just why any particular one should do so is hard to say at the time of purchase, but the group expectancy is favorable, whether the impetus is from an improved industry situation, a takeover offer, a change in investor psychology, etc.”

Warren Buffett Picks a Group of Korean Cheap Stocks in 2004

Approaching the end of the ’60s, Buffett’s asset base was about $100 million. He just couldn’t find enough deep value stocks to keep doing his thing, so he liquidated his partnerships.

Then he started running Berkshire Hathaway (Berkshire) — initially a deep value stock.

It was only after a few years running Berkshire that he decided to look for “wonderful businesses at fair prices instead of fair businesses at wonderful prices."

That’s a whole different approach to investing, since the focus shifts from the group outcome to the individual outcome.

But Buffett still indulges in his deep value ventures every once in a while, for his personal portfolio — just for fun.

In her book, Alice Schroeder masterfully described Buffett’s screening process when his broker handed him a thick book “the size of several telephone directories stapled together” of Korean stocks in 2004.

“Night after night, he leafed through the tome, studying column after column of numbers, page by page. But the numbers and their nomenclature puzzled him. He realized that he needed to learn a whole new language of business that described a different culture of commerce. So he got another book and figured out everything important there was to know about korean accounting. That would reduce the odds of getting hornswoggled by the numbers.”

After that, he began the “screening” process, just like he did back at Graham-Newman. He applied quantitative criteria to separate the wheat from the chaff among this several thousand Korean companies. In the end, he selected a group of a couple dozen Korean deep value stocks.

Here’s Buffett’s remarks about his investment in this group of Korean stocks:

“The future is always uncertain. I think a group of these stocks will do very well for several years. Some of them may not do well, but as a group, they should do very well. I could end up owning them for several years.”

There’s no information about the overall performance of this group of Warren Buffett’s cheap stock picks but it could certainly be in the neighbourhood of 20% compounded annually.

Warren Buffett Cheap Stock Pick: Dae Han Flour

One of Warren Buffett’s cheap stock picks from the Korean stock market was Dae Han Flour Mills (Daehan), a wheat flour producer.

The stock had the following enticing characteristics:

- 25% market share in Korea.

- Book value of 205,000 Won, with 201,000 Won in marketable securities on the balance sheet.

- 18,000 Won in current earnings (2003).

- Price: 40,000 Won.

This was one terrific net net, if you count the firm's marketable securities among its current assets. But, let’s give this firm a closer look.

While it traded well below liquidation value, quality was equally important. You could buy one of the biggest Korean flour mill companies for a price that was two times its current earnings. That’s a very, very low PE.

But then, the price was one-fifth of its liquidation value.

You were buying Daehan’s entire securities portfolio at market price, and the operating wheat flour business for free. Sound familiar?

Daehan was certainly one hell of a net net, and a classic example of Warren Buffett’s cheap stock picks.

This is How Small Investors Should Invest Today

I guess I’ve made my point about investing small sums in the stock market following Buffett’s early investment strategy. These cheap stock picks made Warren Buffett very rich.

Following his strategy of finding cheap stock picks is the way to go for the small private investor.

The strategy consists of buying a diversified portfolio deep value stocks — specifically below liquidation (or "net net") value with a strong qualitative profile.

Net net stocks may look scary — or at best, boring — when assessed individually. But remember — focus on the group outcome. Diversification helps give this strategy its edge.

At Net Net Hunter, you’ll find monthly shortlists of net nets — i.e. stocks selling at prices below NCAV — that meet several selection criteria, most of which are quantitative in nature.

Now, you’d also want to find the kind of stocks Buffett wrote about in The Commercial and Financial Chronicle back in the ’50s. By that, I mean deep value stocks that are also great businesses.

These stocks are rare — very rare, in fact — but they exist.

Using the Net Net Hunter Scorecard, a list of both quantitative and qualitative criteria, you’ll probably find stocks resembling Warren Buffett’s early cheap stock picks. I have, and I've bought them when I've spotted them. (Actually, my biggest mistake has been not buying more of them.)

Net net stocks that meet both the quantitative and qualitative criteria definitely deserve a further look.

Want to learn more? Join Net Net Hunter now to find net nets to stack up your portfolio and boost your long-term returns.

Article image (Creative Commons) by Pictures of Money, edited by Net Net Hunter.