Cheap Small Cap Stocks: Why It's Better to Go Small

Download our net net checklist right now for free. Click Here.

We believe that investing in cheap small cap stocks is a great way to earn outsized returns. Why cheap small cap stocks when so many gurus are buying large or mega cap companies?

The reason is because smaller firms produce higher investment returns as a group, so buying them ultimately yields better performance. This isn’t just our opinion — it’s a data-backed conclusion that any rational investor comes to after a thorough assessment of the facts.

But, why exactly do these tiny companies produce great returns when they’re often unknown, obscure businesses? Well, dear reader, continue ahead and we’ll walk you through the philosophy of investing in tiny, little-known companies. At the end, we’ll even highlight a strategy that’s proven particularly potent for small investors like you.

What Is a Small Cap Stock?

There are many ways to measure the size of a firm, but looking at market capitalization is the simplest way. A small cap stock is a company with a market capitalization below $1 billion USD and above $300 million.

Market capitalization is the company’s current share price multiplied by its outstanding number of shares. This number is constantly changing, but still gives investors a ballpark idea of just how big a business is.

Large cap stocks, the most well-known of the stock market, have market capitalization of +$10 billion US and are included on a major index such as the S&P 500. A small cap company, on the other hand, as per Investopedia, “is generally a company with a market capitalization of between $300 million US and $2 billion,” and also have their own stock indexes such as the Russell 1000.

What Is the Small Cap Advantage?

A well-documented phenomenon called the small cap advantage has been proven to work throughout investing history. This advantage shows that over a long-term period, smaller cap stocks outperform large cap stocks, with the size of the company inversely correlated to its outperformance.

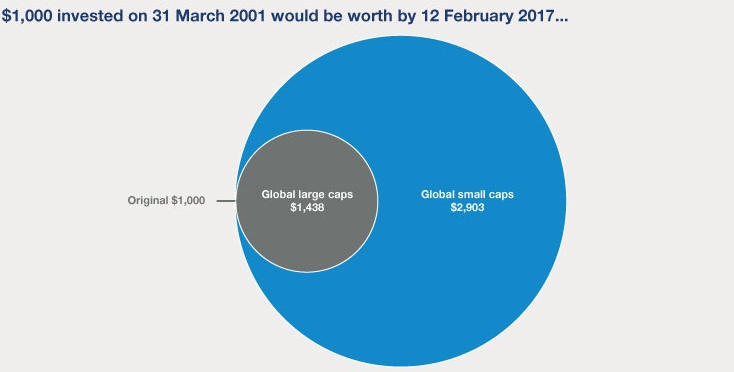

Just look at this diagram from Schroders to really get a sense for the kind of outperformance you may be missing out on by excluding these cheap small cap stocks from your portfolio:

In the chart above, we see that if one had invested $1,000 for 16 years in global small cap stocks instead of global large cap stocks, he would have enjoyed a 102% outperformance! That is doubling the amount of money you could have returned. As you can see, it pays to go for small caps.

The small cap advantage isn’t a big secret either — there have been many studies covering different time periods, geographic areas, and even subsectors of small and large cap stocks to reveal that in the long term, small cap stocks always return a degree of outperformance.

- The Motley Fool studied the returns of both the S&P 500 ETF and the Russell 1000 ETF (the 1,000 smallest stocks traded on the market) and found that between 2000-2019, the Russell ETF returned to investors 312% to the S&P's 226%

- The London Business School found that over 65 years, the British small cap index produced a 3.3% annual outperformance over the FTSE large cap index.

- The Credit Suisse Investment Yearbook 2018 noted that between 1900 and 2018, US small caps annually returned 12.2% compared to US large caps returning 9.9%.

As you see, the advantage has persisted since 1900 and hasn’t been US-specific. There are dozens more studies that you can read from around the globe to see for yourself just how prevalent the small cap advantage is.

Three Key Reasons Why Cheap Small Cap Stocks Outperform

Now that we have explained the advantages of looking into small cap businesses, it's time to take it one step further and look at specific reasons why investing in cheap small cap stocks has produced such positive returns. After all, we don’t believe in following a strategy blindly, but understanding the underlying logic and principles of why a strategy works.

Small Cap Stocks Can Benefit from Big Growth

The first reason has to do with growth. It is much easier for a small cap stock to exponentially increase its revenue in a short amount of time because many of these companies are in their early stages — they have not fully penetrated the market and often have only just started rolling out their product. These companies have room to grow. It’s also much easier to multiply small numbers than it is to multiply large numbers. Smaller firms have a much easier time increasing the sales support needed to achieve rapid growth.

Take the fictional company Tile-By-Design, for example, a small company that recently introduced in-demand tile services in its home state of Texas. Next year, it plans to open stores throughout Arizona, which will double sales but require the firm to double its staff from 200 to 400 people. While a big challenge, it’s very doable under the right leadership. But to grow the firm by 100% the following year, Tile-By-Design would have to roll out to two more states, doubling its personnel from 400 to 800. That’s a much larger challenge. Eventually, the management talent and infrastructure needed to keep doubling will prove too difficult to implement, and the firm will have to reduce its growth rate.

For larger cap companies, it becomes more and more difficult in absolute terms to double its revenue number. There are no analysts on Wall Street predicting Apple to double its $260 billion US in revenues anytime soon, despite how successful the brand and company are.

Lack of Coverage Means Small Cap Companies Are Often Cheap

With such growth potential, you would think that small cap stocks would be widely researched. However, the reality is that these small cap stocks are much less researched — and thus overlooked. This lack of analysis means that the market is less efficient in pricing these smaller businesses. With less competition, it is much easier to find bargain small cap stocks that offer a margin of safety and downside protection.

The reasons for this are two-fold.

1. Time Commitment. There is a limit to how many thorough analyses an analyst can do. An analyst has to prioritise their time, and most likely that priority falls to the large cap stocks and big names. After all, that is where the majority of the interest lies.

2. Illiquidity. Most funds simply can’t invest in cheap small cap stocks, even if they wanted to — and many, such as Berkshire Hathaway’s Warren Buffett, wish they could. Due to their small market cap, these companies’ stock price is much more sensitive to demand.

A big hedge fund of $10 billion US in assets under management isn’t going to bother investing a few hundred thousand on a cheap small cap stock, as the effect on its overall performance is so negligible, it isn’t worth their analyst’s time. Now, let’s say despite this, the fund decides to invest anyway. It would quickly find the stock price bid up so much by its purchase that it would no longer be attractive, and its own upside would have been reduced as a result.

It is also worth mentioning the kind of scenario that occurs after a significant market decline:

You have many high-quality large cap companies suffering big hits to their stock price as collateral damage of a wide market decline. Sometimes the decrease in their stock price is so significant that these high-quality large cap businesses have their market capitalization reduced to small cap levels. If the underlying business is solid and the balance sheet healthy, these situations often recover beautifully once the crisis passes and the market goes back to normal.

Think about a spooked investor willing to sell you Gap, Inc. at a 50% discount, and then him asking you for it back at a higher price once the market has recovered and he has regained his cool. These situations aren’t as rare as you think, as long as you are willing to not let your emotions get the better of you!

In fact, finding these cheap small cap stocks can be quite lucrative. Buying a group of these firms, which are often dealing with a major business problem, is a powerful strategy so long as it's likely that the firm will regain its footing. When a firm overcomes its issue, the stock price also recovers, and countless studies have shown that buying a group of these wounded businesses provides great returns on average — no surprise there for experienced value investors.

One Major Problem with Cheap Small Cap Companies

Before you get out your wallet, keep in mind that buying cheap small cap stocks is not all sunshine and rainbows. In fact, as we saw above, it can require an iron stomach.

Small cap stocks lend themselves to value investing by virtue of the fact that cheap small cap stocks are often the most beatdown equities in the entire market for the reasons we discussed before — small caps are often unfairly punished for the slightest weakness and are often under-researched. These two factors lead to the largest mispricing and best profit opportunities.

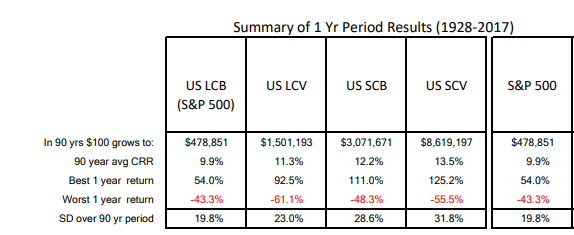

You may have noticed that while small cap value posted the best returns in the above table, they also posted the worst drawdowns and highest standard deviations. Small caps are generally unfairly punished by the market, and value stocks are generally placed in the value category after experiencing a significant drop.

But these statistics are for the general universe of stocks of both small cap and undervalued companies. This can still be a significant number of stocks. From here, you can drill down and then focus on the quality of the cheap small cap stocks within.

Factors that reduce the probability of a cheap small cap stock permanently losing its value — such as debt-to-equity, having a current account surplus, or not selling shares — should be at the top of your list of things to look at.

However, $300 million US isn’t as small as companies get, so what happens when a company’s market capitalization is below that number? They are categorised as microcap (between $50 million and $300 million US), and below that we have the smallest of the small: nano cap. These companies take all the qualities of small cap stocks and push them to the extreme.

Cheap Micro and Nano Cap Companies: When Cheap Small Cap Investing Is Taken to Its Logical Extreme

The relationship between a smaller market capitalization and increased returns doesn’t stop at small cap stocks. In fact, the smaller the market capitalization, the larger the outperformance over the S&P 500 over the long term. The reasons why are the same, just taken to more of an extreme.

In fact, the author of Confessions of a Wall Street Insider, drawing on a study by the University of Chicago Centre for Research in Securities Prices (CRSP), states that “… during a 79-year period, micro cap and small cap stocks outperformed large cap stocks by 437% and 165% respectively.”

We see here that not only do micro cap stocks blow large cap stocks out of the water, they also outperform even small cap stocks by a significant margin. Compounded over a lifetime, that degree of outperformance that you see in micro caps would have been a serious wealth generator.

This shouldn’t come as a surprise. Micro cap stocks enhance every benefit that small cap stocks provide investors, and this applies to an even greater extent to nano cap companies. These are companies that are even more underlooked and under-researched and are even more thinly traded than cheap small cap stocks, leading to more possible volatility. This volatility translates to more sensitivity in their price movements, providing value investors with ample opportunity to buy these companies at a deep discount and profit when their price moves back up.

While on the topic of micro and nano cap stocks, an honourable mention has to be made on a special kind of stock that is generally found in the micro and nano cap sectors that has the potential for huge returns, with additional downside protection not usually found in stocks of this size.

Net Net Investing — Fortune Favours the Bold

If you drill down on the financials of the most beatdown stocks, you will start to notice an interesting situation in some of them — many of the companies will be trading so low that their market capitalization will be worth less than net asset value. Even better, some will be trading for less than NAV, excluding long-term assets. In essence, it is like going to an estate sale, buying up all the furniture, and having the administrator tell you that you can take the house as a thank you gift.

We call these net net stocks — a type of value stock that is so undervalued that it is trading for below its net current asset value (NCAV), and returns on offer from net net investing are exceptional.

We only look for companies trading at a minimum of 67% to NCAV, and the deeper the discount, the better. These companies are cheap micro or nano cap stocks that are the victims of an overblown market reaction. We are betting that the market will see this and price the stock back to at least the value of the assets it holds. The bigger the discount, the more room to go up and the more profit potential we stand to gain. Click for more information on net nets.

The Best Time to Start Is Yesterday

Throughout this article, we’ve discussed a few truths backed up by decades of research and data; The smaller the company, the better the return; value over the long term has beaten growth investing strategies; and finally, that by combining these two well-regarded truths, investors can get the best possible returns out of the market.

Of course, in both cases, there was a caveat: small caps are more volatile, and value stocks can have periods of underperformance. To counter these, we introduced a special kind of cheap stock called net nets that minimised an investor’s downside and has outperformed not only the S&P 500, but small cap and value stocks as a whole. In fact, the strategy’s founder, Benjamin Graham, posted 20% average returns over a 30-year period with his Graham-Newman Partnership focusing on the smallest companies.

If you are going to choose a specific long-term strategy, why would you not choose the best of the best? Ask yourself this: would you choose to voluntarily get a smaller return on your investment?

To get the free net net stock checklist, click here. Start putting together your high quality, high potential, net net stock investing strategy right now!

Article image (Creative Commons) by DarrelBirkett, edited by Net Net Hunter.