Deep Value Investing: Buying A Dollar For 0.60 Cents

Get full access to our VIP Newsletter right now, for FREE. Click Here.

There is a strong argument for deep value providing some of the best long-term returns you can find in the market. Before we talk about deep value, we need to understand what value investing is.

Value investing is simple: Buying a stock that is selling for less than what it is fundamentally worth. But first, you need to decide what the business is worth, and that is where the complexity comes in.

There are many ways to value a business. Some look at quantifiable metrics like book value or price/earnings; others, like Benjamin Graham, whom we will talk more about later, value companies based solely on their hard assets.

Historically, value investing has consistently beaten the market average. So, value investing is good, but what if we could increase our returns by buying the most undervalued and unloved business in the market? That is exactly where deep value investing comes in.

Deep Value Investing 101

What is deep value investing?

Deep value investing is the process of buying stocks or bonds for well below a conservative assessment of their net worth. Two elements are needed -- a large margin of safety and a conservative valuation methodology. Sometimes, as with the case of net nets, the valuation methodology is in itself a large margin of safety.

The main difference between deep value and regular value investing is that these strategies focus on the absolute cheapest stocks in a universe relative to value. Targets have often even been priced for imminent bankruptcy. But, in all cases, the market has turned so pessimistic on the firm that the price has become illogically low… below any semblance of reality. With net nets, that value is a hyper-conservative assessment of a firm's liquidation value. Most firms go on to enjoy decent futures, to the value methodology is in fact too conservative.

Deep value investors make their money by sifting through the market's noise and pessimism to find stocks that the market has mispriced by a much larger margin than the situation warrants. There is also often a perceived increase in risk, which as we will see, may prove an illusion.

As mentioned before, deep value can be broken down into different strategies, many of which are covered by our sister site Value Investing Sage. The better known deep value investing strategies are:

Acquirer's Multiple

Relatively new to the scene of investing strategies, the acquirer's multiple is a valuation strategy designed by Tobias Carlisle, whom we will talk about more later.

The formula is as follows:

EV / EBITDA

Where EV = Enterprise Value = Market Cap + Debt - Cash

The logic behind this valuation method is that it gives a fuller picture of the true cost of acquiring a business. This is because EV includes information such as debt. For a company looking to take over another business, the debt load is a huge factor. This can change a company that is undervalued on a book value basis to overvalued on an Enterprise Value basis and helps investors avoid value traps.

Combining Enterprise Value with an attractive EBITDA (Earnings Before Interests, Taxes, Depreciation and Amortization) yield can produce a list of businesses that would make attractive takeover targets, in which the investor could handsomely profit from the merger.

The strategy is often criticized by Warren Buffett and Charlie Munger, however, along with other major value investors (who often chuckle, calling it "earnings before all expenses"… which is obviously divorced from real business reality).

Negative Enterprise Value

Negative Enterprise Value also relies on EV for finding deep value picks, but focuses on enterprise value that's actually a negative number. This happens when a business has more cash than the combination of the firm's debt and market cap. In these situations, an acquirer would be effectively paid to take over a company.

Generally, deep value investors will find a high quality company that due to temporary circumstances, such as a bear market, has seen its EV go negative. These can generate high returns as these businesses are essentially trading below the value of their cash and have a strong chance of mean reverting back to a normal stock price.

The Walter Schloss Ultra

Walter Schloss is one of the value superinvestors with a long term record rivaling Buffett's own. He loved his cigar butts and often held 100 different cheap stocks in his portfolio at one time. After he moved on from net nets, his ideal stocks were the cheapest businesses relative to book value as well as trading at or near their 52-week lows. The theory being that a diversified basket of the cheapest stocks would take care of themselves as a whole.

The “Ultra” part is our twist which increases returns while decreasing risk. One of the changes to screening is looking for stocks cheap to tangible book value, this stricter criteria that values hard assets only gives investors a wider margin of safety. The second important change is focusing on the firms with either significant share buybacks, insider buys, or strong catalysts. To learn about the Ultra strategy, click here.

Net Nets

Now for our personal favourite (and Buffett’s too), net nets refer to stocks trading at a discount to their net current asset value. This strategy, created by the granddaddy of value investing, Benjamin Graham has continued to outperform since its inception decades ago.

Net Current Asset Value (NCAV) is calculated as follows:

Current Assets - Total Liabilities - Preferred Shares = Net Current Asset Value (NCAV)

This measure provides an investor with an extremely conservative valuation for the business, discarding all assets that are not liquid. In essence, Graham believed that buying companies at a discount to their NCAV was like buying a business that could liquidate itself, pay off all its debts, and still have cash leftover to pay shareholders.

It's not hard to see why this strategy provides such a huge margin of safety, especially when combined with Net Net Hunter’s Core 7 criteria, which helps filter for the best net nets. The strategy also provides some of the best returns available in the market as we will see later on when we compare the returns of deep value strategies.

Is Deep Value Investing Used by Money Managers?

Anyone can write about a strategy and talk about the theoretical upside, but it doesn’t mean much without any proof. Thankfully, deep value has some very well known faces in the investing community who swear by it. In fact, deep value is such a varied category that many of the largest hedge funds have partaken in one strategy or another, from Dan Loeb to Carl Icahn.

For clarity’s sake, we are going to stick to “balance sheet” deep value investors who used strategies similar to those outlined above. This means we are not including activist investors.

Remember, there are no rules that are set in stone, and each one of these investors developed their own style. They have also shifted approaches over time. What they shared was the central belief that the best returns lied in the cheapest and most undervalued stocks that were unloved by the market.

Warren Buffett

No deep value article is complete without perhaps the most famous value investor alive today, and the man who made the term ‘cigar butts’ famous.

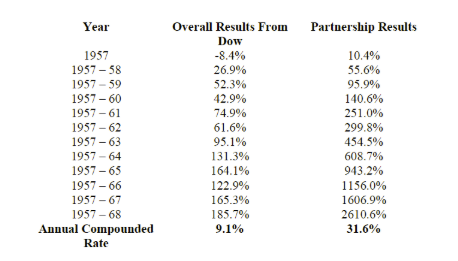

While today Buffett is in the modern value camp, believing in ‘great companies at a fair price,’ it wasn’t always like this. During Buffett's earliest years under Graham’s tutelage and under his own partnership, he sought out the cheapest and most beaten down stocks he could find - ‘fair companies at a great price’ As he put it in his 1989 Berkshire Hathaway letter:

“A cigar butt found on the street that has only one puff left in it may not offer much of a smoke, but the 'bargain purchase' will make that puff all profit.”

These were the classic net nets we spoke about earlier, Buffett would find companies that were trading so cheaply that the upside was immense, meanwhile, most of these companies had a strong balance sheet that would allow it to survive its temporary issue.

There is no doubt that Buffett’s record before his partnership days is amazing, averaging around 50% a year for a decade. The big question is, if Buffett was so successful with deep value investing, why did he stop? We’ll let the Oracle of Omaha explain:

“..I was investing peanuts then. It’s a huge structural advantage not to have a lot of money. I think I could make you 50% a year on $1 million. No, I know I could. I guarantee that.”

Buffett is suffering from his own success, and his large amount of managed capital doesn’t allow him to invest in the normally small companies where one finds deep value opportunities.

However not all large fund managers have given up on deep value investing. Some of the most famous managers continue to beat the market over the long term by sticking to deep value principles and investing in securities that they see are extremely cheap relative to value.

Howard Marks

Showing just how wide the scope of deep value investing can be, Howard Marks, a deep value investor that even Warren Buffett listens to had his start investing in distressed debt, meaning bonds of companies that were being priced for bankruptcy.

As the head of Oaktree Capital Management, a hedge fund that manages $124 Billion Dollars we see that deep value investing isn’t constrained by portfolio size.

As his fund grew, Marks started expanding his horizons to deep value in equities, such as special situations. Howard Marks’ deep value philosophy has clearly paid off, as despite managing one of the largest pools of capital in the industry, as of 2014 produced an average annual performance of 23% over 25 years.

Seth Klarman

Seth Klarman literally wrote the book on Margin of Safety. It is no surprise that this hedge fund manager is a huge fan of Buffett's and has maintained one of the best long term returns for a value investing fund.

Klarman differs from many other value investors in that he puts risk above all else and believes that a large margin of safety is what allows him to keep investing in deep value strategies. The deep value strategies Klarman has used are varied and depend on the opportunities present.

He has invested in bankruptcies, looking to profit from liquidation (similar to Benjamin Graham’s philosophy), as well as distressed debt, spin offs and other more classical deep value strategies of investing in the most undervalued stocks in an index.

The common thread between all these strategies is risk management. Klarman's fund, the Baupost Group, has been known to regularly have between 25%-50% of its portfolio sitting in cash. This isn’t a hard rule though, as during the financial crisis Klarman was famed for investing $100 Million Dollars a day during specific periods.

Klarman’s focus on risk has served him and his investors well, as he has managed a near 20% annual return over 25 years with only one down year. All while a significant portion of his portfolio was sitting in cash.

What Can We Expect From Deep Value?

Now that we have given an overview of a few of the deep value strategies everyday investors can start doing today, and some of the big names that back them up and have built entire careers out of them, it's time to get to the most important part - what exactly are the long term results of using such strategies.

We are unfortunately not all at the same calibre as Buffett, Klarman or Mark -- they may have access to opportunities that we don’t or are, let’s face it, just plain smarter than us. So it is critical to look at the historical performance of these strategies in a standalone quantitative way. Thankfully there have been a number of backtests conducted on the many different deep value strategies out there:

- Between 1999-2017, buying a basket of low price to book value stocks and rebalancing every 12 months would have yielded a CAGR of 14%, already a nice premium above the broad market. However, if you add the extra criteria of the Ultra strategy, and replace low P/B with low price to net tangible assets, investors receive a 17.52% return, widely trouncing the market.

- In a study between 1999-2016, forming an equal weight portfolio of the entire available universe of American Negative Enterprise Value stocks that were rebalanced annually, an investor would have returned 27.45% per year. Unbelievable.

- Finally we arrive at our favourite strategy: Net Current Asset Value stocks. Over a 23-year period between 1985-2007, James Montier reported in his book that holding an international basket of stocks trading below ⅔ of their NCAV would have given you an average return of 35%, a mouthwatering performance.

Additionally, Oppenheimer studied net nets between 1970-1982 and found that they doubled the return of the markets. We expect long term performance in the 20-30% CAGR range.

While it is easy to look at these results and wonder why all investors shouldn't just follow these strategies, a word of caution: These portfolios are theoretical, and can’t accurately reflect how a real portfolio with a human behind it might act.

For example, in the negative enterprise stocks study, there were periods where the portfolio held 350 stocks. Realistically most investors would never do this. Then, if an investor tried to reduce the number of stocks, they would see their portfolio returns decline substantially.

Likewise in the net net study, one thing those returns don’t mention is that 5% of the portfolio suffered a 90% drop or more, almost double the broad market average. How many investors are prepared to watch a drop of that magnitude?

There are all important caveats, these backtests serve to show in an unbiased way that these strategies can produce outperformance.

Deep Value Investing Today

The deep value strategies we have discussed all have significant long term outperformance over the broader market. The key term here is long term. A casual observer may look at the last five year of relative underperformance across all value strategies and assume that value investing is dead.

This couldn’t be farther from the case! As long as human emotions are at play in the market, there will always be value opportunities to exploit, and for those willing to be bold - deep value strategies too.

During these times, investors should always focus on the key that makes every deep value strategy successful: Margin of safety. If you buy a dollar for 40 cents, you are bound to be alright in the end.

To get a free net net stock checklist, click here. Start putting together your high quality, high potential, net net stock investing strategy right now!

Article Author: Isaac Aydelman

Article image (Creative Commons) by kurzkarl74, edited by Net Net Hunter.