Why Guy Spier Rejected Warren Buffett's Investment Strategy

Here's a question: Give the fact that Warren Buffett is the most successful, respected, and wealthy investor of all time, why would any professional value manager reject Warren Buffett's contemporary investment strategy? It's seems odd, but Guy Spier has his reasons.

Who Is Guy Spier?

If the name Guy Spier seems familiar, it may be because of his growing reputation among the value investing community. Spier is famous for paying $650 000USD, along with Monish Pabrai, to have lunch with Warren Buffett. His 2014 book, "The Education of a Value Investor," has also made the rounds and is becoming a very popular book. It's currently rated a 4.5 star read by 295 people on Amazon.

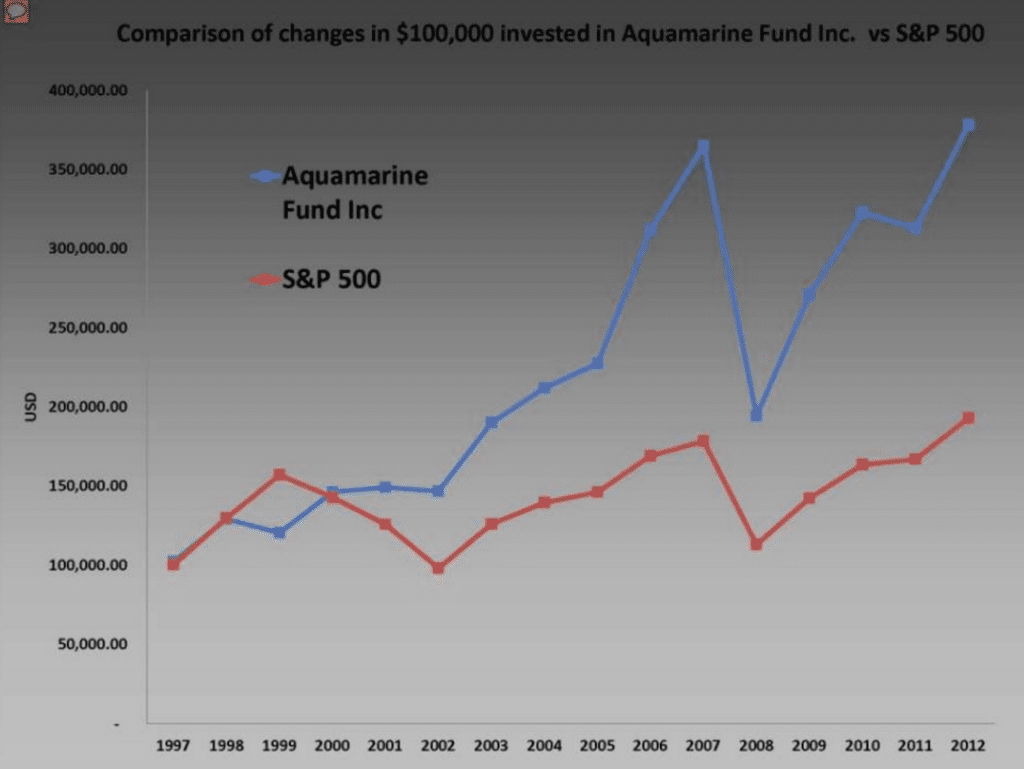

Spier was born in South Africa and educated at the City of London's Freeman School, later receiving his MBA from Harvard. He started out as a professional money manager in 1997 with $15 Million mostly from family and friends. Since then he's managed to wrack up outstanding returns versus the S&P 500. In 2011, his gains totalled 221.6% versus the S&P 500's 36.7%. That's an impressive record especially when most managers fail to beat the market over even a moderate period of time.

Guy Spier's investment vehicle is his Aquamarine Capital, an investment partnership inspired by Warren Buffett's early partnership. Aquamarine is fairly restrictive with regards to who it manages money for, and fund information is only distributed by request.

Citing Buffett, Munger, and Pabrai as major investment influences, you'd be forgiven for thinking that Guy Spier sticks to Warren Buffett's moat-type businesses. While Spier was once a card-carrying Buffetteer, his true preference is for classic Graham deep value investments.

What's Guy Spier's Problem With Warren Buffett?

In 2011, Jacob Wolinsky of Value Walk fame conducted a masterful interview with the man him self, which was published by The Manual of Ideas. Jacob's conversation with Spier revealed some valuable insights into how a small investor should manage his portfolio.

"Pretty soon after I started I fell in love with this whole GARP idea. I spent a lot of time around Ruane Cunniff by researching their ideas and attending their annual meetings, where I had the chance to listen to and meet some of their brilliant investors and analysts, including Bob Goldfarb, Greg Alexander, Jonathan Brandt, and Girish Bhakoo. I learned about why Warren had moved into the business of buying, and paying up for better businesses."

GARP, or "growth at reasonable prices," is a strategy that boils down to selecting companies that are expected to grow at high rates relative to their industry, or businesses in general, and then to buy those firms when their stocks are trading at reasonable valuations. What counts as reasonable is a matter of perspective, though, and many investors are split between using Discounted Cash Flow or classic Ben Graham measure of value.

Just like many other investors who are just starting out in value investing, Spier only focused on Warren Buffett's modern investment strategy, buying growing companies with strong moats at decent prices. He dug deep into Buffett's strategy, dissecting exactly what he looked for when he hunted large, well run, businesses with durable competitive advantages, and then formed his investment partnership around that.

As Guy Spier explains, this sort of strategy has a few major pitfalls.

"Something I learned during the financial crisis was that when you pay up for a better business, you can suffer greatly when the price people are willing to pay for that business goes down dramatically, as it did in 2008. Many “better” businesses fell in price more rapidly than other businesses because, as the crisis came about, many investors were not willing to pay up for growth or quality. ...I lost more money owning those businesses than I would have if I had owned the right cigar butts..."

But large drops in price during bear markets wasn't the only investment trap that Spier spotted. As it turned out, GARP firms also pushed investors into making major behavioural mistakes when investing.

"If you talk about your stocks, it will affect how you think about them as well as the portfolio decisions you make. At the time, I did not believe it would skew my decision making. But if I go back over the life of Aquamarine Fund and examine my letters to investors, I can see clearly how this created a bias for better businesses, simply because it was more fun to talk about them. (Or perhaps a better way to put this is that I developed a bias for businesses that are fun to talk about.)"

If Buffett was right in calling inflation a corporate tapeworm, psychological biases are definitely an investor's tapeworm. They cause us to overestimate the returns we can expect from a particular stock, how fast the company will grow, the profit the company will produce, or even how durable the competitive advantage of the company is itself. This trap is often due to the Halo Effect, the tendency to attribute or overestimate a range of good traits that a company may not actually have based on the existence of a single good trait that actually exists. In dating, for example, a beautiful woman may be seen as more sociable, better adjusted, or more popular, by virtue of her looks when she may not actually possess any of those attributes.

By contrast, Cigar Butts tend to sidestep this issue much of the time. They don't readily lend themselves to producing the halo effect and you're much less likely to talk about them at a party, keeping those psychological and social chains off so you can easily change your opinion when the facts change. They're also known to trigger an investor's gag reflex, so investors systematically underestimate a Cigar Butt's future growth rate and stock return.

Ironically, despite providing investors with better returns, small retail investors prefer great companies to Cigar Butts because they cause less psychological or emotional strain.

"Owning things that Mike Burry says have an “ick” factor or cigar butt investment ideas that have a lot of hair on them is not something your investors want to hear about unless you have a very sophisticated group of investors. In my case, many of my investors had never owned stocks before so they were not going to feel too comfortable about me owning companies with a high “ick” factor. So I was immediately biased toward buying better businesses at a reasonable price. With most audiences, it is much easier, for example, to talk about Heineken and their phenomenal sales growth in Russia and other BRIC countries, or about Nestle and their Nespresso brand, than to talk about businesses that are either “hated, or unloved,” as Whitney Tilson would put it."

Part of the reason why these "dirty" stocks work out so well is due to a phenomenon called "reversion to the mean." Reversion to the mean is a basic law in both life and investing. The principle is that abnormal results, either positive or negative, tend to not last.

Take hight for example. A freakishly tall father and mother will have tall children, but those children will usually be shorter than their parents. The hight of future offspring reverts to the average hight of people in general.

The same principle is at work in investing. It's why Cigar Butts tend to work out well in the end. Inevitably, the company's business improves or some piece of good news comes out to send significantly undervalued shares skywards. Conversely, great returns don't last and firms with higher levels of profitability tend to get beaten back to more average levels of profitability. This is why Buffett loves moats, but even moats can't fend off natural forces indefinitely.

"When I started investing I used screening software to find companies with the metrics you mention — high ROE, low price to book, and high return on invested capital. I was looking for all of those types of things.

I think all of those metrics have a potential downfall, and I will give you an example: In general, you want to invest in high ROE businesses, and you can run various types of a screen to find high ROE businesses, but to the extent that in the vast majority of businesses, ROE is going to revert to the mean, you may have paid up for something that might not be there in five years. The ROE five years forward might be a lot lower than the ROE you are paying up for today."

As Guy Spier explains, you end up paying a large price up front for a business that is facing an immutable law of nature. Eventually, that return on equity will shrink and the business will be far less profitable than when you spotted it. While the risk-reward relationship may still be in an investor's favour, the company's margins face a tremendous amount of pressure.

".........you want to own something that makes the situation unusual and gives you an unusual risk/reward. That is not necessarily a cigar butt, but you have to identify what it is that will result in a return of 3x in two years. I am trying very hard to own things that will give me a return of 3x in two years rather than settle for something that will appreciate at a few percentage points better than the market."

One of the huge advantages of net net stocks, the classic Cigar Butt, is that the risk-reward profile is heavily skewed in the investor's favour. Roughly 75% of net nets produce large positive return over a two year period, and the average results of a net net stock portfolio over time is 15% over and above the market. That makes for a 25%+ annual average return.

Often investors new to net nets make the mistake of only buying a few stocks and assuming that they'll all see massive advances in price. This is just not the case. While net nets work out well, some stocks are bound to disappoint which means that a proper net net strategy requires a decent amount of diversification. Still, net nets are probably safer than you assume. James Montier found that these stocks only see major (90%+) losses in 5% of cases. That compares to 2% for stocks in general, showing just how safe a well diversified net net stock portfolio is versus the market.

Keeping in mind basic requirements of good net net stock picking (no Chinese firms, resource explorations firms, etc) the highest returning net nets are often the stocks that are selling for the cheapest prices relative to net current asset value (NCAV). Buy cheap enough and you can bag the 3x advance in 2 years that Guy Spier favours.

But, as he explains, price to value often isn't enough.

"Tom Russo has said, “flying an airplane requires you to focus on five or more instruments,” and you can’t favor the altimeter over the speed indicator, or the vertical speed indicator over the pitch indicator, for example. You have to look at all the instruments together and fly the plane integrated. Tom has used this plane analogy to discuss investments. There is no single metric you should look at but rather keep an eye on all of them."

This is why investors should be using a high quality scorecard when assessing their stocks. For my own investing, I use our Core7 Scorecard to help dissect the net net stocks that I buy to see if they're the sort of stocks that are bound to avoid losses and produce meaningful returns. I've compiled most of the thinking that's gone into this checklist into my net net stock guide, Retire Young & Rich. Ultimately, it takes more than blindly following Buffett's current strategy to produce the best possible investment results. As Guy Spier said,

"Thus, you could say that my approach to investing, in contrast to Buffett, has gone in the reverse direction. My approach today has become more similar to the way Warren Buffett invested when he got started. The important thing to realize is that if Buffett today was running a fund the size of Aquamarine, he would be investing differently than the way he does today."

Get the free net net stock essential guide. No obligation, no risk, no spam, just our free net net stock essential guide you can use. Enter your email address in the box below right now.

Read next: Are Warren Buffett's Moat Companies Really Great Investments?