Cheap Japanese Stocks Deliver Outstanding Returns

Download our net net checklist right now for free. Click Here.

There is no argument that serious long-term investors should stick to value investing. It remains one of the oldest investment strategies still followed today. There are countless studies showcasing its outperformance of the broader market over the long term. Unfortunately in the last decade, there has been a drought in good value stocks.

However, many are only looking at the American market. Companies such as Toyota, Sony, Softbank — some of the world’s largest and most well-known companies come out of Japan. The country has one of the largest and most stable economies in the world, but along with the heavy hitters, there are also undervalued companies just begging to be discovered. It begs the question, why aren’t you looking to the Land of the Rising Sun for cheap Japanese stock opportunities?

In today’s world of ultra-high valuation and the United State’s record bull market, investors find it harder and harder to uncover high quality undervalued stocks in America. Because of the lack of options, investors either give up on the strategy due to poor returns, settle for lesser-quality stocks or create a portfolio that is far too focused and undiversified. All of these lead to underperformance in the long term.

It is ironic then, that many investors who are so desperate for a high return or more high-quality value stocks seem to suffer from tunnel vision, refusing to look abroad for their value picks when there are so many great alternatives with cheap Japanese stocks.

Why Are Japanese Stocks Cheap?

The reason for the huge concentration of undervalued stocks in Japan has much to do with general pessimism surrounding Japan’s market. But don’t be fooled — we have already learned from Benjamin Graham that Mr. Market’s skepticism is our gain.

You see, many large investors are afraid of investing in Japan because when they look at the Tokyo Index, they see a scary stock chart that shows a big drop, with a very slow recovery.

In fact, Japan’s stock market as a whole still hasn’t reached its historic high from 1989 — that is almost three decades of stagnant growth! Besides that, Japan also boasts one of the highest debt-to-GDP ratios in the developed world.

As I mentioned before, if you look deeper into the headlines, you will see that Japan is not the apocalyptic nightmare as the news paints. It is precisely because of this pessimism that so many great value plays remain hidden in Japan.

A Country’s Margin of Safety

While there are many metrics to value stocks, such as price to equity, price to book and net current asset value, have you ever considered using these metrics on a stock market as a whole? For example, if we use the classic price to book ratio (market capitalization/carrying assets on its balance sheet) and apply it to the S&P as a whole, we get some interesting information.

The S&P 500’s price/book ratio stands at 3.55, quite a bit higher than its historical median of 2.77. Its recent low was at 1.78, at the bottom of the great financial crisis. Compare that to Japan’s stock index (the Nikkei 225 at 1.78), and you start to see the contrast in value between the two markets.

That's just incredible — on an index-weighted basis, the Nikkei today is as comparatively undervalued as the S&P was at the bottom of a recession.

Is it no wonder why there are so many more undervalued, cheap Japanese stocks compared to American stocks?

We also often talk about having a margin of safety when investing in companies. If you would like additional confidence in investing abroad, why not look at it from a macro point of view and see the margin of safety that Japan as a country provides?

Japan’s Nikkei 225 is the third-largest exchange in the world behind the United States’ big two (New York and NASDAQ). Many people seem to forget that Japan’s economy is massive ($4.9 trillion GDP). An economy of this size simply cannot crash and evaporate overnight, like what may happen in some emerging markets.

While the debt burden is high, what is different about Japan compared with most of the developed world is that this debt is mostly held onshore by Japanese citizens. This small detail gives the Japanese central bank a lot of leeway in dealing with its debt.

A low crime rate combined with one of the most efficient infrastructures in the world aids Japan in keeping its huge economy ticking. A perfect example is how fast Japan rebounded after it succumbed to a tsunami and nuclear disaster concurrently. When looking at net nets, we love to see how the net net handled hard times in the past; I would say, not many countries would have handled disaster as well as Japan has.

Finally, there is one extra risk every investor needs to keep an eye on when investing internationally, and that is currency risk. A nation’s currency collapsing can wipe out all of an investor’s gains — and that’s the best-case scenario! The Japanese yen, however, is seen as a safe-haven currency; whenever there is fear in the market, it is one of the currencies that investors pile into, as well as the US dollar and the Swiss franc. This status provides an extra moat for investing in Japan.

Value Investing on Steroids

With such a low price to book value, it should come as no surprise that there are a significant number of cheap Japanese stocks on offer. Most classic value investors would opt for low price to book stocks, since it’s the most widely known method of stock selection.

Historically, classic value investors investing in cheap Japanese equities have fared extremely well despite the market disaster. You just need to know where to look.

Now, what if I told you there was a different way to invest based on value? A way that has statistically been proven to have a higher annual return rate than simply buying stocks that appear cheap based on metrics like book value or price to earnings ratios?

This may sound like a sales pitch, but this strategy is about as old as value investing itself; in fact, the “father of value investing,” Benjamin Graham, invented it and published it for the world to read!

If that’s not enough, there was one Graham follower who got his investment career started following this strategy — amassing an annual average of 29% over nearly ten years — who once said:

“A cigar butt found on the street that has only one puff left in it may not offer much of a smoke, but the ‘bargain purchase’ will make that puff all profit.”

As it turns out, this investor is quite well-known today, being none other than Warren Buffett! He was one of the first to open a fund based on Graham’s strategy of looking for cheap stocks trading below their net current asset value (net net investing).

Net Current Asset Value (NCAV) is calculated as Current Assets − Total Liabilities. This gives the investor a very conservative estimate of a company’s liquidation value. This conservatism adds to their margin of safety and downside protection. On top of this, Net Net Hunter also recommends following a number of criteria that research has shown provides an increase to long-term portfolio returns.

You simply look for a stock whose price is trading below its NCAV by at least 67%, as recommended by Graham — the larger the margin, the better the discount.

What makes Graham’s net net investing strategy so effective internationally is that its core principles are so simple, they can be applied to any stock market with a strong rule of law and transparency in numbers.

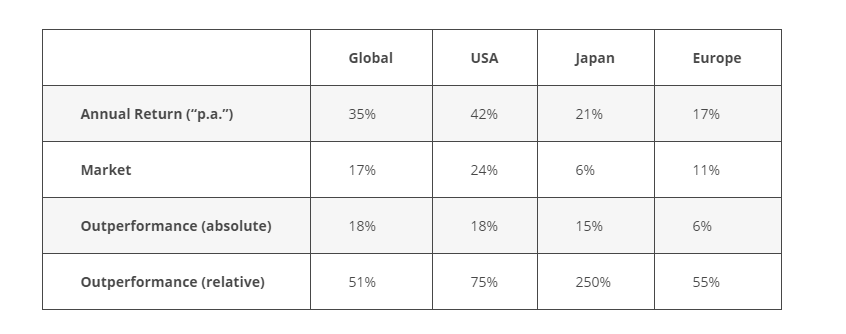

Despite the American bias, one study by James Montier on international net nets saw that between 1985-2007, an international basket of net nets returned 35% per year against 17% for an equally weighted basket of the total market (small-, mid- and large-cap equities). That means you could have doubled a passive investor’s returns just by looking abroad. What is even more important, though, is that Montier continues:

“Currently I can find somewhere around 175 net-nets globally. Interestingly, over half of these are in Japan.”

If you want to catch such returns, it would serve you well to fish where most of the fish are! From Montier’s study, we learn that not only has investing in international net nets provided historical outperformance, but also that much of this outperformance comes from cheap Japanese stocks.

Leader Electronics Corp

One great example of an amazing net net success story out of Japan is Leader Electronics Corp. We brought up this cheap Japanese stock in May 2017 as an example of the mechanical Ansam strategy. It proved to be a fantastic investment as, after six months, the stock popped 80%, followed by another 80% increase a few short months later. These kinds of sharp rises are only seen in net nets, and in order to get probability on your side, you want to make sure they are of high quality.

Leader Electronics first got our attention thanks to it passing all of the Core 7 criteria and then some! It was one of the cheapest relative to NCAV stocks on our shortlist, boasting a 55.8% discount, no debt, a huge 10x current account ratio and, finally, a positive NCAV burn rate (NCAV increased q/q and y/y). All of these factors provided a huge margin of safety, protecting investors from the possibility of suffering a permanent loss of capital.

In the end, this net net covered all the bases as far as our core criteria are concerned and then some. A timely investment in this company would have more than paid off, as its price reached its NCAV within six months and has remained above it since!

Felissimo Corp

In April 2017, another cheap Japanese stock was on our net net radar — the mail-order business of Felissimo Corp, which was then in the middle of a transition from a paper-based to a web-based model. Soon after we covered the stock, it started an upswing that led it to finishing the year up 30%!

While the stock never did rise all the way up to its intrinsic NCAV, which would have been an 83% rise, those who followed the Ansan strategy would have sold after 12 months and booked that 30% increase. Keep in mind that 2017 was a year where the S&P returned 21.14% and most so-called professionals lagged behind it in performance!

While this cheap Japanese stock passed all of our core criteria, it did have some flaws that decreased the margin of safety we seek. The company had not had adequate earnings for some time — a sign that this could be a perennial net net. However, there was a lot to like about the company, along with the catalyst of a huge share buyback that made it ripe for a popup, turning this into a classic Buffett cigar butt from his partnership days.

Like with Leader Electronics, because of the language barrier, a mechanical strategy such as the Ansan strategy is advised. With Felissimo it was even more crucial, as an inexperienced investor might have waited for the company to reach its NCAV, which it never did, and would have missed out on the last few puffs from that cigar.

Shinko Shoji

For another example of how following Net Net Hunter’s core criteria could have lead investors to stellar returns with a cheap Japanese stock, we can look back to 2014 and find Shinko Shoji. This company had been in the electronics distribution industry since 1953, with most of its business being in Japan itself.

The stock was beaten down badly during the great financial crisis, and due to increased competition and suboptimal economic conditions in Japan. To the uninformed, this stock looked like a loser, having most of its value evaporated and struggling to regain its footing. But, it was trading at a healthy 46% discount to NCAV. This was enough to get net net investors interested in a closer look, and there was a lot to like.

While increased competition had decreased its margins, Shinko Shoji had remained profitable for the last 5 years, even providing investors with a consistent dividend. In fact, its NCAV had been steadily growing, a sign for a financially healthy company. Despite being in an inventory-heavy business such as electronics, Shinko Shoji had such a healthy current account ratio at 3.3, and on top of this carried a tiny debt-to-equity ratio. All of these factors showed that this company had a lot of downside protection, and a good margin of safety - the backbone to any net net investing.

So that is the downside covered, what about the upside? Well, there was plenty to like there, too. In that year Shinko Shoji had just completed a sale of its subsidiary, that would be reflected in future earnings reports, and had just signed a new distribution deal with an American company, increasing earnings in future. Besides that, at that point in time the electronics distribution industry of Japan was in a period of consolidation, and Shinko Shoji’s combination of undervalued stock, low debt and healthy balance sheet would make it a prime target for a buy-out. This was the kind of situation Buffett thrived off of in his partnership days.

In the end, Shinko Shoji’s NCAV target would have given investors a 91% profit. While it did reach its original NCAV in 2018, investors following the Ansan strategy would have sold after a year, for a very healthy 39% profit.

Art Vivant

For my last example, I want to call your attention to Art Vivant, a cheap Japanese stock in the art industry that is a perfect example of how quickly a net net can shoot up in value and generate in a couple months, what many investors will not see over the course of an entire year!

Art Vivanti was a net net trading at a huge 50% discount to NCAV, was healthily growing its net current assets and was growing its income. It had also saved this income in the form of a healthy current account surplus. Thanks to its huge discount and downside protection, this was another perfect candidate for a cigar butt investment. In fact, months prior, rampant speculation had caused the price to shoot up on news of a new app the company was developing, before the price settled back down again.

Two months after publishing our analysis, the stock shot up 54% in two months, once more on speculation. It settled lower again, but above our buy price. The stock moved steadily higher and eventually even reached its NCAV 3 years later for a total 101% increase. This is why pays to buy the dip!

Land of the Rising Net Net

While I explained the advantages of investing in Japan over the United States and other international markets with net nets, it is still important to be aware of certain Japan-specific issues that could affect your investing.

The most obvious is the language barrier, compounded by the fact that most Japanese companies do not post any English financial reports. However, thanks to technology, we can get the gist of financial reports — and thankfully, numbers are still numbers regardless of language! In addition to this, there are constant innovations in the translating space, with programs and sites utilising deep learning to provide ever-more accurate translations!

While yes, this means that a lot of qualitative data will remain out of reach, we can safeguard our portfolio by using a mechanical strategy that banks on the collective returns of high-quality net nets as a whole. This means relying on the quantitative data, having a defined entry/exit rules, and good diversification.

Another point Japan has been criticised for is its corporate culture, which tends to favour stakeholders (employees, directors) over shareholders. While this may have been true in the past, the tide is turning today. On the back of increasing frustration from shareholders in Japanese companies, shareholder proposals have more than doubled since 2011!

An additional way of circumventing this possible issue is to look for companies with a catalyst that would benefit stakeholders as well as shareholders. Catalysts such as stock buybacks, selling of company assets or introducing a share compensation structure all align the interests of both classes. Why fight the stream when you can invest with it?

You Too Can Become a Cheap Japanese Stock Wizard

Thanks to today’s technology and the competition it has created between brokers, investing outside of your home market has never been so easy, and getting over barriers such as language and culture becomes simpler every day thanks to translation apps and the internet for information.

From 1985-2007, the S&P 500 had an annualized return of 9.36%. What would a basket of international net nets have returned over the same period? 35%.

You owe it to yourself to make use of this great opportunity and take advantage of others overlooking cheap Japanese stocks and their opportunities because it “seems” difficult. The average investor wouldn’t dare invest outside of his home market, and many professional investors look at the news and wouldn’t dare invest in Japan. But Buffett said it best — be greedy when others are fearful.

You might see apprehension, but I see a lack of competition. And where there is a lack of competition, I can enjoy a better edge and better returns!

To get the free net net stock checklist, click here. Start putting together your high quality, high potential, net net stock investing strategy right now!

Article Author: Isaac Aydelman

Article image (Creative Commons) by Japanexperterna.se, edited by Net Net Hunter.