Why Does Net Net Investing Work So Well?

In 1975, ben Graham revealed that his net net stock strategy performed so well, he eventually renounced every other value approach to focus on net nets exclusively. Evan has made learning Graham’s strategy his life focus since 2010, and has compiled a comprehensive overview for small investors. Download Your Essential Net Net Stock Guide for FREE. Click Here.

Ben Graham summed up the secret of sound investing with three words: Margin of Safety. Net net investing may be the only strategy that follows that advice to the letter.

What is a net net?

A net net is a stock selling for a price well below its net current asset value (NCAV) -- i.e., the value of current assets less total liabilities, preferred shares, and off-balance sheet liabilities.

Of course, they are cheap for a reason -- usually more than one reason. Net nets are so hated and forgotten that, sometimes, the only good news is the absence of bad news.

Then again, Benjamin Graham earned around 20% per year just buying hundreds of these sub-liquidation stocks for more than three decades.

Why do net net stocks work out so well?

Before we get to that, let me show how well they actually work.

Returns On Offer For Net Net Investing Strategies

I was sitting behind the computer desk in our home office years ago busily skimming listings of journal articles trying to find studies looking at Benjamin Graham's low price to NCAV investment strategy. The more I looked, the more amazed -- and baffled -- I felt.

The following table summarizes the results of some of these studies:

| Author(s) | Name of the Study | Period Studied | Net Net Portfolio Annual Return |

| Oppenheimer, Henry | Ben Graham’s Net Current Asset Values: a Performance Update | 1970-1983 | 28.2% |

| Greenblatt, Bruce et al. | How the Small Investor Can Beat the Market | 1972-1978 | 40% |

| Carlisle, Tobias et al. | Ben Graham's Net Nets: Seventy-Five Years Old and Outperforming | 1983-2008 | 22.42% |

| Goebel, Joseph | Net Current Asset Value, Financial Distress Risk, and Overreaction | 1971-2007 | 32.83% |

| Montier, James | Graham's Net Nets: Outdated or Outstanding? | 1985-2007 | 35% |

This table summarizes the results of different studies showing the returns on offer for a net net investing strategy. (Source: Produced in-house by the team of NNH)

Annual returns in excess of 20% per year, and way above the market average are the rule for net net investing strategies in different time periods, according to academic research. But this is not only a theoretical expected return. Superinvestors like Warren Buffett, Peter Cundill, or Walter Schloss, to name a few, earned such spectacular returns investing in net nets.

Why Do Net Net Stocks Work Out So Well?

Given that net nets are the market’s debris, it just seems incredible that they offer such spectacular returns.

Why do they work so well?

Here’s a list of reasons I’m going to walk you through in this article:

- NCAV is the most conservative valuation metric.

- Reversion to the mean tilts the odds toward net net investors.

- The good news effect.

- Net nets are excellent takeover candidates.

- Liquidations benefit net net investors.

Net Net Investing: The Question Of Conservatism

Unlike price, value is a very subjective thing -- the variety of valuation methods available attests to that.

First of all, you have relative valuation metrics. If a retail business is trading at 5x price earnings ratio (PE) and all of its peers are trading at 15x, you can say it is relatively undervalued. However, if you’d done that during the late 1990s, and early 2000s you could’ve bought a "cheap" internet trading at 30x PE -- only because its peers were trading at 60x PE. Sure it might have been relatively undervalued at the time but, when internet stocks tanked, knowing that they narrowly missed losing 98 or 99% of their money would have been cold comfort.

Absolute valuation methods, on the other hand, estimate the value of a business on its own merits regardless of how the market values its peers. Following Warren Buffett’s advice, most investors try to find businesses with moats that will earn outstanding returns above the cost of capital overtime and can reinvest those profits to grow at the same rate in the long term.

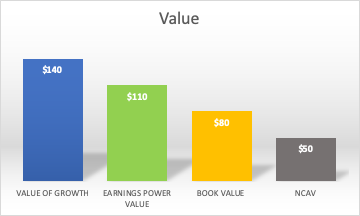

The “value of growth” is the accurate measure for such wonderful businesses -- e.g. Coca-cola or Amex --, but it is based on the assumption that they will grow and reinvest profits at those spectacular rates for a long time. On the other hand, there are many small or medium size niche businesses with barriers to entry which earn above average returns on capital but can only reinvest in growth up to a certain point -- e.g. See’s Candies. In their early stages, growth is valuable for these businesses.

However, paying for “cheap” growth that just isn’t so -- i.e., buying “the next McDonalds” that’s just another burger store -- only leads to spectacular losses.

For the average business -- the one with no barriers to entry --, growth has zero value because it won’t earn a rate above the cost of capital. Hence, the average business is worth only some multiple of its current or average earnings. Since the market has an average PE of 15x, stocks trading for multiples below that would be cheap -- or so the theory goes.

Now, what if earnings collapse? After all, future earnings are uncertain. In that case, investors turn to book value, looking for solid ground.

Valuing a business based on it’s stated book value can be grossly inaccurate, though. The market value of land, real estate, or machines is rarely close to their stated book value.

After growth, earnings, and long-term assets are gone, what’s left?

That’s right, current assets. A dollar of cash is always worth a dollar. Receivables and inventory are less reliable but usually not as much as goodwill or property, plant, and equipment.

So it comes as no surprise that Ben Graham argued that the most conservative valuation method consisted on subtracting the value of all liabilities to the value of a firm’s current assets, valuing long-term assets at zero.

The conservative nature of NCAV makes it less subject to downward revisions. Growth and future earnings can turn out to be pumpkins and mice, but cash and inventory are what they are. This valuation method itself gives the investor a solid margin of safety.

Net Net Investing And The Mean Reversion Effect

Aside from the ultra-conservative valuation, net nets have to be cheap to provide an additional margin of safety -- ideally, a price lower than two-thirds of NCAV.

But don’t just focus on any particular net net. The interesting thing about these sub-liquidation stocks is that they’re so dirt cheap as a group, that the odds are stacked on your favor -- they’re either worth at least their liquidation value, or they should just close shop and return capital to investors. This systematic mispricing puts a mean reversion mechanism in motion that makes extraordinary returns possible.

What is regression to the mean?

Regression to the mean is a statistical phenomenon by which initial sampling errors diminish as repeated or larger samples are taken. For example, there’s a 50/50 chance of getting heads or tails on the toss of a coin. Toss a coin 10 times, and you’re likely to get a skewed 30/70 or 40/60 distribution of outcomes. Toss it 1,000 times, though, and the distribution will be very close to the 50/50 distribution. This is a pervasive phenomenon in nature -- extreme outcomes tend to revert towards the mean overtime.

In the stock market, very strong downward price movements are followed by similarly strong gains, and vice versa -- the stock market reverts to the mean. When stock prices divert so far from fair value that they edge below NCAV, sooner or later they are bound to bounce back to NCAV, because businesses can’t be worth more dead than alive for too long.

Waiting for the stock market to revert to the mean takes discipline, since it could take years to work out -- for some people, that’s as fun as watching paint dry.

Net Net Investing And The Good News Effect

To be trading below liquidation value just means the market expects a net net to go bankrupt sooner or later. Thus, by definition, net nets are usually hated or feared.

Infosonics is a great example. It sold cell phones in South America during the 2000s. Some countries imposed a big tariff, and it lost huge sales. It had a solid balance sheet but it wasn’t profitable. I found Infosonics in 2013 when it was facing yet another blow: a patent infringement lawsuit. It traded at $0.56 in November, when I bought it with a 51% discount to NCAV, net cash, and no debt.

A month later, management issued a press release announcing a new distribution partnership with Ingam Micro. With this news, investors came back and the stock price went to $1.40. I doubled my money and sold then but, to my horror, the NASDAQ reinstated the stock back on the index next week and shares peaked at $4.50, only to settle back at $2.50 a couple weeks latter.

Such large price movements only happen to firms that are very depressed. Much like a thumb pressing a spring, good news slide the thumb off it and send the stock price skyward.

Net Net Investing: Takeovers And The Value Effect

Value investors usually make their valuations, buy at a discount, and then wait for the market price to match their value assessment, trusting the mean reversion mechanism will work out to prove them right. But when a third-party takeover occurs, they actually get to see how accurate their estimate of value was.

For net net investors, a takeover often means outsized returns since they paid so little. Indeed, business takeovers are agreed upon by informed parties and they’d never agree on a price below liquidation value for a going concern.

But, who’d want to buy a troubled business? Most acquirers assume they can do a better job than the previous management, or they want to grow just for growth’s sake, or they think they can extract “synergies” out the purchase. Whatever the reason, net nets are ideal takeover candidates because their balance sheets are very solid.

Also, takeovers are more frequent among net nets than among other stocks. This is yet another reason why net net investing works out so well.

Net Net Liquidations Are Profitable, But Infrequent

Given that net nets are worth more dead than alive, it makes sense that net net investors hope their stocks to close down -- yet, that’s not usually the case. In fact, in my ten years as a net net investor, I’ve never bought a stock that liquidated later.

However, liquidations do provide net net investors with a solid cushion to fall back on. Having bought at a discount to NCAV, net net investors are likely to profit in this worst-case scenario as well.

Net Net Investing Strategy: The Quintessential Margin Of Safety In Practice

All of the above reasons should be enough to make my point: buying a group of net nets is the quintessential margin of safety in practice.

They have little debt, so they can whether extreme market conditions without going bankrupt. They are cheap relative to an ultra-conservative valuation metric, so the odds of overpaying for them are infinitesimal. Net nets as a group activate the mean reversion mechanism in the market, tilting the odds to the side of the investors. If that wasn’t enough, net nets are great takeover candidates and are usually acquired for prices way above NCAV. Last, but not least, even in the rare event of a liquidation, if you paid below NCAV you’ll probably earn a profit.

There’s a catch, though. Net nets are hard to find, and some of them deserve their price. At Net Net Hunter, each month we comb through a raw list of 1,000 net nets from around the world and select a Shortlist of 50 high-quality net nets for our members. You can sign up for a full membership here or Click here to get a free net net stock checklist.

Article image (Creative Commons) by Matthias Ripp, edited by Net Net Hunter.