The Shipping Industry Cycle Is Turning: Any Net Nets Around?

Net net investing was Ben Graham's strategy of choice and even helped Warren Buffett earn the best returns of his career. Get our Essential Net Net Stocks Guide to understand this strategy in detail. Click Here.

If you're set on investing in cigar butts with extremely large upside potential, the upcoming shipping supercycle may be for you.

I’ll be honest with you — cyclicals are usually not my thing. I focus on net nets — dirt-cheap stocks selling below liquidation value. You don’t need to forecast the economy or have an opinion about the industry outlook of a particular net net to do well. Just buy a group of them over time, and you’re likely to make 20% a year in the long run.

Cyclicals are a whole different animal. To profit from them, you need to buy very solid firms at the bottom of the cycle and then ride the wave up. Buying high at the peak or buying too early in the downturn will almost certainly be recipes for disaster.

But then, can you actually spot the bottom of the cycle? Most of the time, you can’t. There are just too many variables in place. But sometimes, all the variables point in one direction, and you’d be crazy not to give it a closer look. That’s the case with the shipping industry in December 2019.

In this article, I’m going to walk you through the dynamics of the shipping industry cycle, give you hints about where we are in the cycle right now, and show you how it could unfold in the near term. I’ll also give you advice on how to pick the shipping stocks that are most likely to do well. Read on!

Shipping Industry Basics

What is the shipping industry?

The shipping industry refers to the transportation of goods by ocean-going ships with high capacity.

The shipping industry is generally made up of three segments: container, bulk transport, and tankers. The container shipping segment transports containers — i.e., large metal boxes of a standard design and size — filled with goods ranging from laptops to bananas to cars.

The bulk transport shipping segment refers to the movement of significant commodities such as iron ore, coal, or grain in bulk.

Finally, the tanker shipping segment carries liquid cargoes such as oil, liquefied gas, and various chemicals, also in bulk.

The shipping industry is enormously important to our modern globalized economy as roughly 90% of goods are transported by sea.

The Basics of the Shipping Industry Cycle

Ironically, shipping is a terrible business, and investors are better off avoiding it — most of the time.

Ships carry goods across the oceans at a price called the “charter rate”. Supply and demand determine this price, and no carrier has a moat to protect its business against these forces. Ships are just commodities.

As more and more people around the world are lifted out of poverty and join the middle class, they demand consumer goods. As you can guess, ships are needed to transport those goods from one place to another. This secular growth trend in demand is affected by short-term events like civil wars, recessions, natural disasters and the like.

To serve that demand, carriers need ships. But, unlike cars or trucks, building a ship takes about two years, and after they join the global fleet, they stay in service for around 20 years. So, when there’s a sudden surge in demand, and supply isn’t ready to serve it in the short term, charter rates shoot up — and a sudden drop in supply has the same effect if demand doesn’t fall accordingly. The sudden price spike attracts large amounts of capital that are soon invested in new ships. When those ships join the global fleet a couple of years later, they create excess supply, and charter rates drop. Because ships stay online for at least two decades, the imbalance usually lasts for long periods.

Now, the average container ship is priced at around $10 million, and oil tankers cost around 4 or 8 times that figure. For that reason, shipping firms need both debt and equity to finance their assets. Shipping firms usually have very high financial leverage. They usually carry high operating leverage as well.

(What is operating leverage, you might ask? Operating leverage is simply the amount of fixed operating costs any specific business bears. Compare this to financial leverage, which is the fixed financial cost of any business — i.e., interest on debt.)

To stay afloat — no pun intended — during the bad times managers of these businesses usually issue more shares and dilute existing shareholders.

Constantly declining revenues, high fixed costs, and diluted property mix together to form a perfect capital-destroying bomb. With all these obstacles in place, late in the shipping industry cycle downturn, both lenders and investors are understandably tired, and they stop throwing their money away. Capital becomes scarce, and shipyards stop building ships.

When the number of scrapped ships exceeds the number of new ship orders, supply is set to fall. Charter rates shoot up — often a few months in advance — and the shipping firms that survived the previous carnage eventually return to profitability. Because of the high fixed costs, revenues in excess of the break-even point flow straight down to the bottom line, earning shareholders tidy profits for as long as the recovery lasts.

This attracts fresh capital, new ships are built, and the cycle starts over.

The Shipping Industry Cycle: Finding Value at the Bottom

Of course, during a shipping industry cycle downturn, the market punishes shipping firms with very low prices, sending some of them even below liquidation value.

Liquidation value is just the “fire sale” value of a company’s assets less all liabilities. There are at least two approaches to measuring liquidation value, one more conservative than the other. The first — and more conservative — is net current asset value (NCAV); the second is net asset value (NAV). NCAV is the value of current assets less all liabilities, while NAV equals the value of all tangible assets — both current and fixed — less all liabilities.

Benjamin Graham first used NCAV as a proxy for liquidation value and argued that if you could buy a group of stocks selling for less than two-thirds of NCAV, you’d make a decent 20% annual return in the long term — his own experience proved his point. But when net nets became scarce, value investors such as Warren Buffett, Walter Schloss, and Peter Cundill turned to stocks selling below NAV with very good results.

So, what if you could buy a group of shipping stocks selling below NCAV just before the cycle turned around? That would be the perfect, yet unlikely, scenario. A positive NCAV is a privilege of companies with either huge cash piles or zero debt — usually both. While Net Net Hunter does list some shipping stocks on our screens, you typically won’t find many net nets among shipping firms. What you can find, though, are shipping stocks selling below NAV.

Shipping firms’ assets are mostly — you guessed it — ships, and liabilities are just huge piles of long-term debt often secured by those same ships. Much like NCAV, NAV is a proxy for liquidation value, so a shipping stock selling below NAV should at least catch your attention.

Can you catch shipping stocks at the bottom of the cycle, though?

The Shipping Industry Cycle: Can You Call the Bottom?

When looking into the shipping industry, you should keep an eye on supply and demand, then ask yourself whether you can predict major shifts in either one of those variables.

Forecasting demand is hard, while assessing supply is simple. If you search the web, you’ll find data about the number of ships comprising the global fleet, their average age, and the number of ship orders.

If you spot an event that will clearly reduce supply in the short term, while keeping demand constant — or even increasing — you can predict that charter rates will surge in the short term with a high degree of certainty.

The Shipping Industry Cycle: Where Are We Now?

Right now, we just bounced off the bottom of the shipping industry cycle. Now, why do I say that?

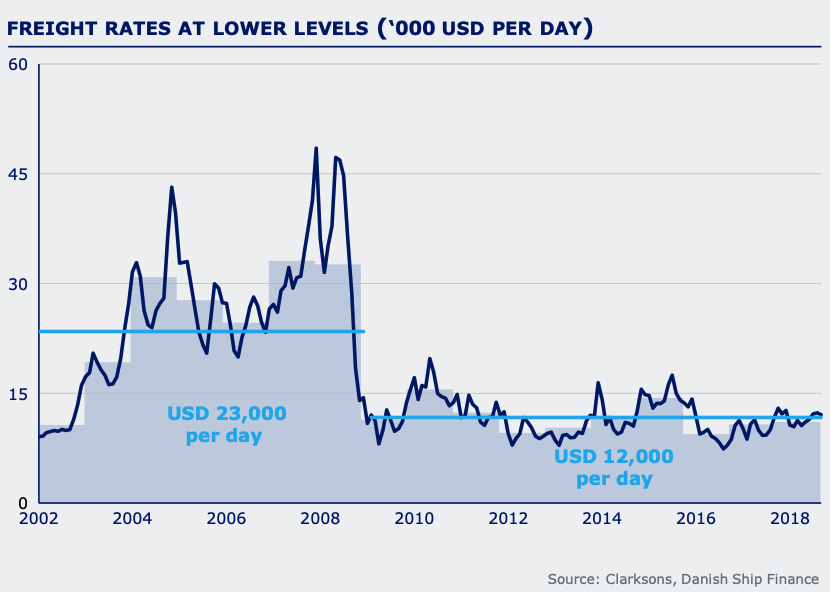

Up until the early 2000s, shipping had been through a downturn with the usual overcapacity, firms declaring bankruptcy, and both lenders and investors losing significant sums of money. The International Maritime Organization (IMO) had issued a rule for the phaseout of single-hull tankers, and firms had been ordering double-hull tankers in advance to be ready when single-hull tankers actually left the fleet. In the meantime, the coexistence of single- and double-hull tankers crushed charter rates. (Remember, tankers are ships that carry either crude oil or refined oil products.)

Now, when the IMO finally ordered an accelerated phaseout of single-hull tankers effective before the year 2003, there was a sudden dearth in vessels — i.e., a sharp fall in supply. Demand also picked up during the global recovery that followed the dot-com bubble crash.

This supply/demand cocktail shot charter rates to the sky, prompting a shipping industry bull market that lasted until 2008.

To get some perspective on this previous bull market and the bear market that followed, take a look at the following chart for “freight rates”:

Today, we have a somewhat similar situation. A couple of years ago, the IMO issued a new rule ordering all ships and vessels either to run with low sulfur fuel or install scrubbers on their fleet to burn traditional high sulfur fuels effective January 1, 2020. This new rule alone will take at least 2% of the global fleet out of the sea for some months — because ships will be sent to the shipyard to install the scrubbers — effectively reducing supply in the short run and pushing charter rates up.

But, won’t the sudden spike in charter rates prompt a new shipbuilding spree? Not likely. First, shipyards have been going bankrupt for some years, so there are fewer shipyards available. Second, the ones that are still alive are either installing scrubbers on used ships now or are going to be installing scrubbers next year.

Capital available to the industry is also in short supply, and the facts even now point to a structural reduction in capital available. On the one hand, shareholders suffered terribly as stock prices have been crushed and management has sold an increasing amount of stock at fire-sale prices just to keep firms alive. You can hardly call management smart capital allocators. The fact that a ship is typically only profitable for two years during its useful life certainly doesn't help. Legacy shareholders are understandably tired of this business after 10 long years, so purse strings (particularly from hedge funds and the like) have been pulled tight.

To make matters worse, new bank regulations (Basel III) are also tighter, preventing banks from lending aggressively to industries like shipping. These regulations, in force since 2018, require banks to increase liquidity and reduce financial leverage. Shipping firms have shifted financing to the high-yield bond markets in order to obtain the needed financing. In short, the cost of capital for the shipping industry is high.

All of this comes as demand for ships is set to increase. The trade dispute between China and the US is one reason. Sorry, what now? Doesn’t that just push down global demand for goods? Not really. If the ongoing negotiations between the countries result in a permanent agreement that ends their trade war, expect demand for goods to skyrocket.

Even if the talks fizzle out, while governments on both sides would like to think that they can curb demand for foreign goods, the truth is they can’t. Exporters just find ways to send their products to the same destination, usually routing goods through other countries. The funny thing is that this situation only makes ship routes longer and, thus, more expensive.

In sum, a sudden supply drop is probably coming January 1, 2020, just as demand is set to grow.

The Shipping Industry Cycle: What You Should Look for in Shipping Firms

Now that you’re bullish on shipping, let me put your feet back on the ground. While the industry fundamentals are clearly recovering, forecasting is always anything but accurate.

There could be a global recession, capital could flood the shipping industry once again or the IMO could end up extending the deadline for new rules to be effective — in short, my analysis could be flawed, or downright wrong. If that’s the case, it would be disastrous for investors mistiming the market.

You need a margin of safety. First of all, buy way below NAV — preferably below NCAV if possible.

You should also look for firms with enough cash to survive until the cycle turns. Too much debt is a big no-no as well, but don’t expect zero-debt firms. Also, remember that leverage is a big plus if there’s a recovery. If management is buying shares aggressively, that’s a good sign.

If you’re really bullish on shipping, you could also invest in integrated businesses such as charterers and shipbuilders, because they’ll certainly benefit from a bull market in shipping as well.

Take Richfield International, a firm that offers brokerage services for shippers. The stock showed up on our Shortlist in 2015, before a previous much smaller industry upturn. This company was listed in Australia and was a tiny nano-cap, a penny stock selling for $0.085 AUD per share, while net current asset value (NCAV) per share was at $0.17 AUD. Charter rates had a sudden increase that year, and this stock returned 400% in just 12 months. Or Conrad Industries, a small American shipbuilder with very low debt, currently selling below NAV.

Anyways, even if you buy a group of high-quality shipping stocks selling below NAV and the bull market unfolds, don’t hold for too long. Should you sell at NAV or at a multiple of NAV? Whatever gets you through the night, I guess.

Charter rates for tankers have been picking up since September, and shipping stocks — especially in the tanker sub-sector — are returning to NAV levels.

Take Scorpio Tankers, for example. Current price is close to NAV, and it’s the largest, most efficient product tanker operator in the market. Members of the Net Net Hunter Inner Circle have been discussing Scorpio and other very cheap firms in the shipping industry, and most of the ideas discussed in this article have been discussed there in depth.

If you want to find high-quality net nets in the shipping industry from around the world, join us now!

Disclaimer: I don’t own stock in any of the companies mentioned in this article. This article contains my opinion on this subject, but should not be viewed as financial advice of any kind.

Article image (Creative Commons) by Bernard Spragg. NZ , edited by Net Net Hunter.