Net Net Value Investing: Making Money Out Of Junk

Get our Essential Net Net Stocks Guide to understand this strategy in detail. Click Here.

Net net value investing is a spectacularly profitable -- yet, somewhat disgusting -- investing strategy. But, what exactly is it? And how did Ben Graham use net net investing to earn the highest returns of his career?

Why is net net value investing disgusting? Well, the strategy reminds me of a TV show I used to watch -- back when we all enjoyed cable TV -- called “Extreme Cheapskates”.

The show portrays the lives of individuals who live very frugal lives, often just for cheapness sake. I remember one of these individuals actually went to the dumpsters in a back alley next to a fancy restaurant to pick up lobster leftovers on weekends, which she then “re-cooked” at home with herbs she planted. It was a “free” lobster meal, after all, and she seemed to enjoy it.

Eventually, most of these extreme cheapskates retired young and rich, but the process was gruesome.

Net net value investors are the extreme cheapskates of the financial world -- picking among the market’s trash for free value. As you’re about to see, many value investing gurus have found that the strategy is enormously profitable when managing small sums.

What Is Net Net Value Investing?

Price is what you pay, value is what you get -- or so the saying goes.

The only way to know whether you’re getting a bargain or paying too much is to know what things are worth. For value investors, figuring out what businesses are worth is their main task; paying a sufficiently low price is the rest of it.

Most professionals in the financial industry use the discounted cash flow (DCF) method to estimate intrinsic value. DCF consists on estimating the future cash flows of a business and then discounting them by an appropriate discount rate. However, for the average business, future cash flows are essentially unpredictable, and discount rates are anything but exact figures. Hence, DCF is a very unreliable valuation method.

Instead of counting your chicken before they hatch, you could just count your eggs, so to speak -- that is, you could value the business assets as they stand here and now and then subtract all liabilities to arrive at a simple book value figure. However, since accounting rules mandate firms to record the book value of fixed assets like property, plant, and equipment, or buildings, and land, at their historic cost -- i.e., the acquisition price -- less accumulated depreciation, the recorded values of these assets are seldom close to their actual market values. Nevermind the book value of intangibles, which could actually be worth zero in the market, but are still recorded at cost on the balance sheet.

Benjamin Graham was well aware of the flaws in valuation methods. After giving it much thought, he concluded that the most reliable and conservative valuation metric was liquidation value.

What is the liquidation value of a business?

The liquidation value of a business is the value of the firm’s current assets less all liabilities or net current asset value (NCAV). Stocks selling below NCAV are called net nets.

What is net net value investing, then?

Net net value investing is an investing strategy that consists on buying net nets.

What’s The Point Of Investing In Net Nets?

Investing in net nets is not only very profitable, it is virtually safe.

Net Net Investing Is The Most Conservative Investing Strategy

Buying at a low price relative to an ultra-conservative valuation gives the investor an ample margin of safety. Owning a basket of stocks purchased at such low prices just adds safety to the strategy.

Graham considered net nets a “class of undervalued stocks”, which means they had a fairly predictable behavior as a group -- he owned around 100 at some point. While any particular net net could fail by going bankrupt or losing its value over time, on average, they offered spectacular returns.

Take the odds in a roulette game. When you bet $1 on a single number and win you’re paid $35. But you have a 37 to 1 chance of losing so, even if you bet $1 on each number at the same time you’ll end up losing money. Now, let’s say you were paid $39 if you won on a $1 bet on a single number. In this case, you would have a small advantage on every single bet against the house, and the certainty of winning $2 on every spin of the roulette simply by betting $1 on every single number. Buying buckets of net nets puts the investor in the latter position, giving him a small -- but certain -- advantage on every purchase he makes, and making it almost certain he’ll win on average in the long term.

Returns On Offer For Net Nets Are Spectacular

In his 1963 letter, Warren Buffett told his partners that this approach yielded very “favorable” returns. Buffett himself earned 30% per year on average investing in net nets for the 13 years he ran his partnerships. Benjamin Graham earned 20% per year on average buying these sub-liquidation stocks for more than three decades. Walter Schloss earned an average of 16% for four decades buying net nets. Extraordinary returns at a very low risk to be sure.

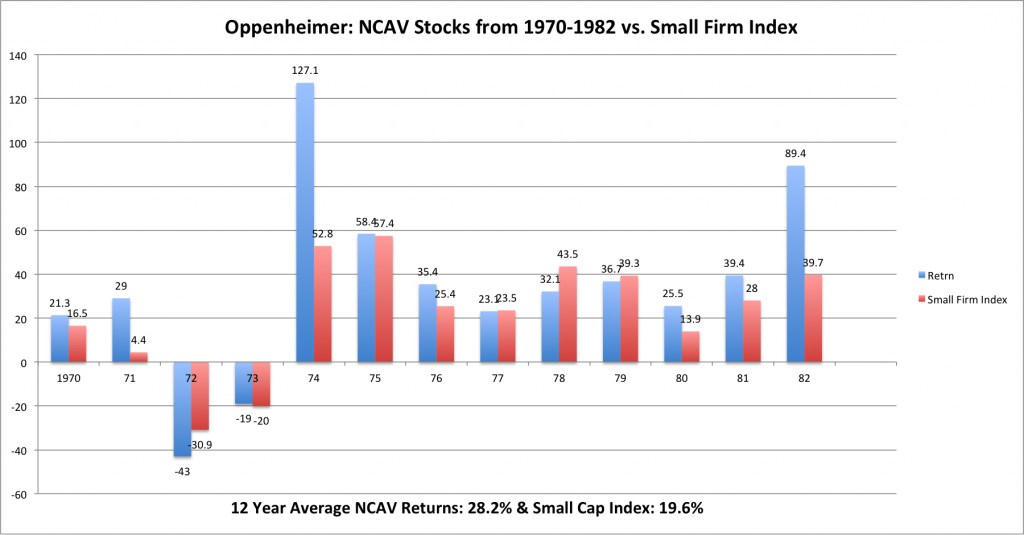

Academic research supports these superinvestors’ experience too. First came Henry Oppenheimer with a paper published in 1984 called Ben Graham’s Net Current Asset Values: A Performance Update. Backtesting a net net value investing strategy from 1970 through 1983, the hypothetical portfolio yielded a 28.2% average annual return.

In 1978, Joel Greenblatt published How the Small Investor Can Beat the Market concluding that a portfolio of stocks bought below NCAV from 1972 to 1978 would’ve earned a 40% annual return before tax. A more recent study by Tobias Carlisle showed that a portfolio of net nets returned an annual 22.42% since 1983 and until 2008. The list of studies is longer, but you get the point -- incidentally, I haven’t found evidence contradicting the previous conclusions.

Not only is net net value investing the most conservative investing strategy available, it is the most profitable investing strategy as well!

Net Net Value Investing: Two Ways To Measure Net Nets

So, net nets are stocks selling below liquidation value -- but, who in his right mind sells a running business for less than it value in a fire sale?

Graham said NCAV was a proxy for liquidation value. As mentioned above, NCAV is the value of current assets less all liabilities. Of course, he realized such a valuation was only a “rough measure” of the value of a business in a “fire sale” scenario.

Net Net Working Capital Stocks vs. Net Current Asset Value Stocks

While the book value of receivables and inventories is close to a market value, in a “fire sale” scenario even these seemingly solid values are punished. Keeping that in mind, Graham proposed adjusting the value of current assets as follows:

- Cash is valued at 100%, since a dollar in cash is worth a dollar.

- Receivables are valued at around 80% of their book value.

- Inventories are valued at around 66% of their book value.

- Long term assets valued at roughly 20% of their book value.

Then, subtracting total liabilities would give the analyst a net net working capital (NNWC) figure. (Source: Security Analysis, 7th ed.)

However, NNWC is harder to calculate because it requires a more in-depth knowledge of the business, its industry and so forth.

Also, a basket of NNWC stocks doesn’t perform much better than a simple net net portfolio. At least that’s Jae Jun’s conclusion after he backtested these strategies and compared their returns. As it turns out, both strategies perform equally well in the long run, but just looking for NNWC stocks -- i.e., stocks selling below NNWC value -- limits the options available at any time -- since all NNWC stocks are net nets but not all net nets are NNWC stocks. In any case, NNWC calculations are prone to error as well, so they’re not worth the additional effort.

Net Net Value Investing Strategy: Why Do Stocks Sell Below Liquidation Value?

Still, why would anyone sell a running business for less than its liquidation value?

Investing decisions are often moved by emotions rather than objective reasons in the short term. Some of the emotions behind those decisions are greed and fear.

A rising stock market or any particular stock moving up attracts new investors just like honey to the bees. People just don’t want to miss on that ride to riches in the short term. But, as always, things eventually turn sour, and fear takes hold of the market. Some investors don’t mind selling below liquidation value, since fear just has them believe everything will go bust sooner or later.

Sometimes stocks sell below liquidation value because there’s a forced seller on the other side. Take index funds, for example. When a stock is thrown out of an index, they just have to sell the stock at whatever price they can get to comply with their investing policy.

In any case, why would anyone throw fresh and perfectly cooked lobster into the dumpster? Who knows? Maybe that someone didn’t feel like eating lobster after he ordered it, or maybe he ate too much bread before the main dish arrived, or maybe he was just tired of eating lobster -- after all, eating too much of anything can make you sick.

I mean, there are many reasons why people would just throw away stocks -- or lobster. Net net value investors are just not picky when it comes to value. We don’t mind stepping inside the dumpster looking for our free lunch -- after all, that’s how Buffett became a millionaire.

Incidentally, Buffett dubbed this sub-liquidation stocks “cigar butts”. They resemble a soggy cigar butt left on the street with only one puff left. You can pick it up, and take that last “free puff” -- it’s disgusting, but still free.

Limitations Of A Net Net Value Investing Strategy

Net nets have their limitations, of course.

First of all, net net value investing only works with very small sums. Net nets are usually found among the small or micro cap universe. When you’re managing more than $50 or $100 million you just can’t pick up these bargains. Small mutual funds manage around $1 billion, and they hold around 50 stocks at any given time. For regulatory reasons, they can’t hold more than 10% of the stock of any particular firm they invest in. Assuming they have equally weighted positions, each position has to be of around $20 million. Now, the total market capitalization of most net nets is below $100 or even $50 million -- they’re also highly illiquid, so building a $20 million position on a stock with a $100 million market cap is virtually impossible.

But net nets are very volatile creatures too. They behave in line with the market, with very large drawdowns during market crashes. Spectacular returns arise every once in a while, of course, but you have to stay fully invested through good and bad times to reap the fruits.

What I’m trying to say is, you need patience -- and an iron stomach -- to succeed as a net net value investor.

Net Net Value Investing: Final Thoughts

Net nets are dirt cheap stocks selling at very low prices relative to an ultra-conservative valuation measure. A basket of net nets offers returns above the market average and superior to most other value investing strategies available.

Also, remember that, for structural reasons, net net value investing only works with small sums. Last but not least, a net net portfolio can be very volatile, and you have to be willing to see large drawdowns before you reap the profits.

Just like the “Extreme Cheapskates”, you can’t be picky. Net nets are ugly, deceased, and forgotten stocks. Here’s the catch -- they’re hard to find.

At Net Net Hunter, each month we comb through a raw list of 1,000 net nets from around the world and select a Shortlist of 50 high-quality net nets for our members. You can sign up for a full membership here or Click here to get a free net net stock checklist.

Article image (Creative Commons) by Rick Kirby, edited by Net Net Hunter.