Are Net Net Working Capital (NNWC) Screeners Worth It?

Download our net net checklist right now for free. Click Here.

Are net net working capital screeners worth it?

If you’re reading this, you probably know that net nets are stocks selling for a price below net current asset value.

Also, you probably know that investing in a group of net nets was Ben Graham’s favourite — and most profitable — investing strategy.

Well, net net working capital (NNWC) stocks are net nets whose current asset values are further adjusted downward.

So, you’d think that buying stocks at discounts to NNWC would yield higher returns than buying at a discount to net current asset value — after all, they’re just cheaper net nets.

Actually, it’s not that simple.

You’d be better off investing your limited time conducting further research to find high-quality net nets.

Net Net Working Capital Explained

Asset values are always more reliable than earnings figures. Current asset values are also more reliable than fixed asset values.

If there’s $1 million in cash on the balance sheet and $40 million in real estate, you can be sure about the value of the cash, but not about the value of the real estate — it could be lower or higher by a wide margin.

That’s one of the reasons Graham loved buying companies selling for prices below their net current asset value (NCAV) — i.e., the value of current assets less all liabilities and preferred shares.

Because current asset values are almost undisputable, a stock with a price below NCAV is almost certainly a bargain.

Graham earned a 20% compounded annual growth rate (CAGR) for about 40 years investing in a group of net nets.

But even among current assets, cash is more reliable that inventories or receivables — especially in the event of a liquidation.

Graham knew this and, in some cases, he would adjust the value of current assets to arrive at NNWC value.

NNWC represented the value of the company in a “fire sale” scenario.

Graham proposed the following adjustments to arrive at an NNWC figure:

- Cash values are not adjusted.

- Take between 75% and 90% of the value of receivables.

- Take between 50% and 75% of the value of inventories.

- Subtract total liabilities and preferred stock.

The exact adjustment to receivables and inventories depended on in-depth industry and company analysis, though. It was not just a mechanical formula.

For example, Warren Buffett used NNWC to value Dempster Mills back in 1961, but he controlled the company and knew what the appropriate adjustments were.

Of course, for any specific stock, you’d rather have a price below NNWC than just below NCAV.

Does that mean that you should only screen for stocks below NNWC?

Net Net Working Capital Screeners: Don’t Waste Your Time, and Money

There are around 40,000 listed companies in the world today, publishing financial reports at least twice a year.

Screeners filter stocks according to specific quantitative criteria. They’re very useful tools for investors.

Valuable screeners cost some money, though.

Is a net net working capital screener worth it?

I believe not.

First of all, net net working capital screeners can’t capture the qualitative measures involved in an NNWC valuation.

As I said, it takes in-depth research and business judgment to determine the appropriate discounts applicable to each company’s current assets.

Inventory dynamics vary between industries. Receivables are even very business-specific — two businesses in the same industry can have very different clients, each of them with their own credit risk.

In other words, net net working capital screeners can’t accurately adjust current assets.

But there’s a more compelling reason to avoid net net working capital screeners altogether: NNWC stocks simply don’t outperform good old net nets.

That’s right.

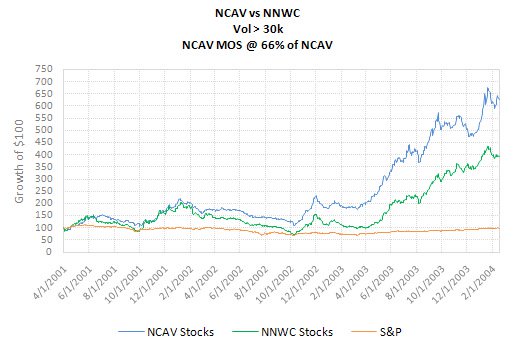

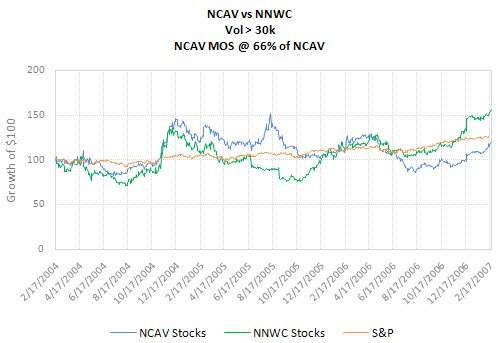

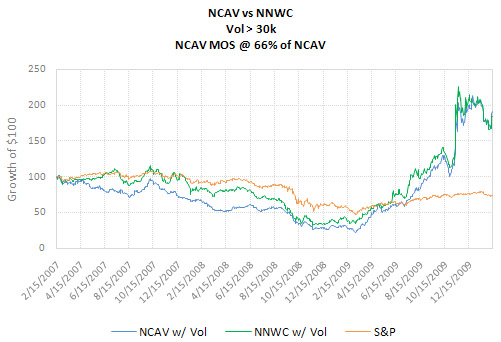

Jae Jun performed a backtest comparing the returns for NNWC stocks and net nets in different time periods.

His results are revealing.

Take a look at the following graphs:

- 2001-2004 period:

- 2004-2007 period:

- 2007-2010 period:

Take a look at Jae Jun’s study here.

Jae Jun concludes that “as long as you buy them with a margin of safety [i.e., at a price two-thirds or less of NCAV], NCAV stocks look to perform equally well.”

Keep in mind that all NNWC stocks are net nets — i.e., stocks selling at two-thirds or less of NCAV — while not all net nets are NNWC stocks.

So, let’s say the universe of net nets in a given period is 1,000, and just one-third of those are NNWC stocks.

A net net working capital screener would only limit your options without increasing your chances of boosting your returns.

It’s just not worth it.

But there’s a way to actually find the best net nets — net nets with increased statistical chances of boosting your returns.

Boost Your Returns With High-Quality Net Nets

Instead of spending your time trying to make accurate adjustments to current assets to arrive at an NNWC figure, conduct thorough research on net nets to look for qualitative traits that actually increase your odds of earning high returns.

When Buffett and Walter Schloss worked for Graham back in the ’50s, they just pored through the manuals looking for stocks selling below NCAV. It was a very basic “screening” process.

After they’d shortlisted these net nets, they’d dig a little deeper to find qualitative traits in them that could boost their returns.

At Net Net Hunter, we’ve spent hours and hours reading Graham’s books and articles, Buffett’s Partnership Letters, and a number of scientific studies about net nets.

What we discovered is that most net nets are cheap for a good reason, and those are the ones you should avoid like the plague.

However, there’s statistical evidence showing that net nets with certain quantitative and qualitative characteristics have a high probability of earning above-average returns — we call them high-quality net nets.

Regarding high-quality net nets, Graham wrote:

“Common stocks that (1) are selling below their liquid-asset value, (2) are apparently in no danger of dissipating these assets, and (3) have formerly shown a large earning power on the market price, may be said truthfully to constitute a class of investment bargains. They are indubitably worth considerably more than they are selling for, and there is a reasonably good chance that this greater worth will sooner or later reflect itself in the market price. At their low price, these bargain stocks actually enjoy a high degree of safety, meaning by safety a relatively small risk of loss of principal.” [Security Analysis, Sixth Edition, by Benjamin Graham and David Dodd, The McGraw-Hill Companies, 2009, p.570.]

So, how do we find these high-quality net nets?

Net Net Hunter has access to a database from which we extract stocks selling below NCAV around the world. This is called the Raw Screen.

Each month, we spend more than 20 hours combing through the approximately 1,000 stocks on the Raw Screen by hand in order to come up with the best investable net net stocks to focus your research on.

We screen stocks based on “Buyability” and “Investment Quality Factors.”

There is no point including a stock on our Shortlist if you can’t buy it. That’s why we look for stocks with at least $1,000 average daily volume and a minimum price. That’s “Buyability.”

Investment Quality Factors include a two-thirds discount to NCAV per share, low debt to equity ratio, low burn rate — i.e., the company is not eating up its value — a small market cap, and a current ratio above 1.5x, among others.

The result is the monthly Shortlist we send to our members.

Looking for high-quality net nets among the Raw Screen is like hunting for deer in the forest, while looking for them among the Shortlist is like hunting in the zoo.

Now, among the net nets you’ll find in the Shortlist, you can run further analysis by using our Scorecard to find high-quality net nets.

Indeed, aside from core quantitative criteria, the Scorecard adds some key qualitative criteria you should look for. For example, there’s evidence showing that the existence of an activist investor increases the chances of unlocking value for shareholders — that’s a catalyst.

We also like to see insiders busy buying the stock at cheap prices — or even share repurchases.

The qualitative assessment requires a high degree of business experience and knowledge on your part, though. Not all activist investors actually end up unlocking value, and the extent to which they can act depends on the jurisdiction where they’re located.

I mean, the Shortlist is a great place to start your hunt for high-quality net nets, but you have to do your own qualitative assessment after that.

Lucky for you, at Net Net Hunter we also have a section with very valuable learning resources to help you get the knowledge required to make accurate qualitative assessments.

Start putting together your high quality, high potential, net net stock strategy. Click here to get free net net stock checklist.

Article image (Creative Commons) by Marco Verch Professional Photographer and Speaker, edited by Net Net Hunter.