Your Low Price To Tangible Book Value Guide

In 1975, ben Graham revealed that his net net stock strategy performed so well, he eventually renounced every other value approach to focus on net nets exclusively. Evan has made learning Graham’s strategy his life focus since 2010, and has compiled a comprehensive overview for small investors. Download Your Essential Net Net Stock Guide for FREE. Click Here.

Tangible book value is a reliable, straightforward, and very conservative valuation metric — yet very few investors use it.

Using less conservative valuation metrics usually lead investors to overpay for businesses. In the long term, this is a recipe for financial disaster.

Intelligent investing, as Charlie Munger said, is all about buying something for less than it’s worth. The less conservative your value estimation is, the lower your chances of actually buying something for less than it’s worth.

In this article, we’ll discuss the advantages of using tangible book value to measure a company’s intrinsic worth and how you can form a portfolio with low price to tangible book value stocks to achieve outstanding returns.

We’ll also show you an even more profitable investing strategy that’s also based on tangible book value.

Low Price to Tangible Book Value: First, Forget About Discounted Cash Flows

So, how do you know if you’re buying something for less than it’s worth?

Stocks are just “pieces” of businesses. When it comes to stocks, what matters is the value of the underlying business.

There are different business valuation methods available.

Since John Blurr Williams published The Theory of Investment Value in 1938, the financial community came to the conclusion that the value of any business was equal to the present value of its future cash flows.

So, most analysts use the discounted cash flows (DCF) valuation method today. What they do is estimate the cash that a business will generate for the following 10, 20 or more years, and then discount those future cash flows using an adequate interest rate.

While this makes sense in theory — since any business consists of a group of productive assets — in practice, DCFs are seriously flawed. Indeed, for most businesses, not even next year’s cash flows are predictable. That’s just the nature of the game. Thus, projecting cash flows 10 or 20 years into the future is nothing but an act of faith.

Of course, businesses that enjoy some sort of long-term competitive advantage usually have steady cash flows, and on these very rare occasions, a DCF would be useful. That’s the kind of business that Buffett buys, by the way.

Also, the discount rate is a very subjective figure. It involves estimating the weighted average cost of capital. Inputs for this calculation include the stock implied volatility and a “risk-free” interest rate — let’s stop there.

How should we measure the value of the average business, then?

Low Price to Tangible Book Value: The Value of Hard Assets

Whether they sell goods or services, all businesses need assets in order to create their products. What’s left for the company after products are sold and expenses are paid is profit or loss.

As we’ve seen, future profits or losses — future cash flows, in general — are usually unpredictable. No company owns its future cash flows yet.

But companies own their assets, and the value of those assets is recorded on their balance sheet.

The value of a firm’s assets less all its liabilities is called book value (BV). This is also known as the shareholders’ equity. BV is a good measure of value. Of course, if you find a business selling for a price below BV, it could be a bargain — not all assets are born equal, though.

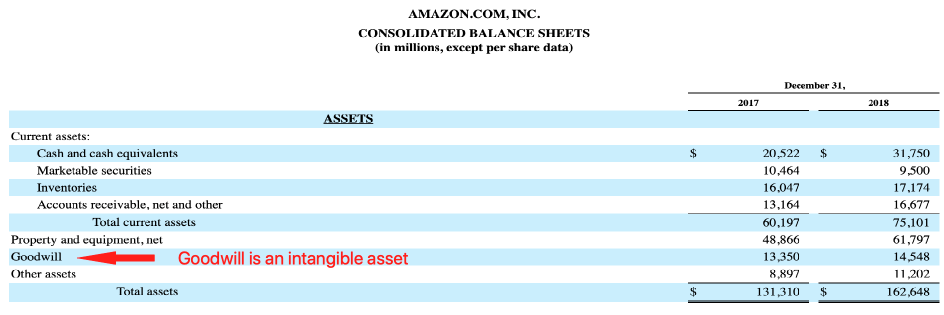

Take a look at Amazon.com’s assets on the balance sheet, for example:

While cash, securities, inventories, account receivables, and property, plant, and equipment physically exist outside the balance sheet, goodwill doesn’t.

What is goodwill?

Goodwill is an intangible asset. If Company A buys Company B, all assets and liabilities of the latter merge with the former at book value. But if Company A paid a price above BV for Company B, then that excess value goes to an account called goodwill.

Besides goodwill, intangibles could be software licenses, patents, or brands.

A conservative valuation method consists of excluding intangible assets from the calculation of BV to arrive at tangible book value (TBV).

TBV is a very conservative valuation measure, much more reliable than simple BV, and certainly way more reliable than a DCF. Indeed, DCF value could be off by a very wide margin — future cash flow projections will be wrong, and the discount rate could be wrong. BV could also be off because intangibles add noise to the figure. But TBV is the likeliest to be very accurate.

In other words, while a low price to DCF value won’t tell you if a stock is cheap or not, a low price to tangible book value stock certainly deserves a closer look.

Low Price to Tangible Book Value Stocks: Focus on the Group Outcome

Let’s say someone offered you a bet on the toss of a coin. Heads, you would give him $100; tails, he’d give you $200. Given that the pain of loss is psychologically twice as powerful as the joy of winning, you’d probably decline that bet since there’s a 50 percent chance you lose $100.

However, if you took the same bet 100 times, your chances of losing any money would be only 0.0004%.

If you find a company selling for a price 50% below TBV, you’re probably looking at a very troubled business — stocks are usually cheap for a reason. The upside is interesting, though, since tangible book value is a very conservative valuation metric.

Since, more often than not, stocks selling below TBV recover, owning a group of them actually increases your chances of earning a decent return.

By adding bets where the probability of permanent loss is smaller than the probability of gain, the overall risk substantially decreases. Adding similar bets on a portfolio of low price to tangible book value stocks actually places the odds on your side.

Focus on the group outcome, and you’ll do alright.

Low Price to Tangible Book Value Stocks: Expected Returns

Academic research regarding the results of a group of stocks selling below TBV is scarce.

However, there are plenty of studies covering low price to BV stocks. Given that TBV is a more conservative valuation metric than BV, there’s reason to argue that a stock selling for a low price to TBV would be even bargain if analyzed in relation to BV.

On Tweedy, Browne’s study called What Has Worked On Investing, researchers found that, among the stock indexes, the smaller companies selling at the lowest prices in relation to BV offered the best returns — well in excess of the market average with a 23% annual rate.

Also, the team at Broken Leg Investing ran some backtests and found that buying stocks with a 60% discount to TBV returned a 27.5% CAGR during the same period!

Low Price to Tangible Book Value: There’s Something Even Better

Expected returns for stocks selling below BV or below TBV look impressive, but there’s something even better than either metric: net nets.

What are net nets?

Net nets are stocks selling for a price two-thirds below net current assets value (NCAV) — i.e., the value of current assets less all liabilities.

It’s like calculating tangible book value, but among the tangible assets, you only include the most liquid ones in your valuation.

NCAV is a proxy for the liquidation value of a company. That’s what you’d get if the company liquidated tomorrow.

This is the most conservative valuation metric available.

If you find a stock selling for less than its liquidation value, then you’re probably getting a bargain.

Academic research shows that buying a group of net nets massively outperforms other investing strategies, including low price to BV and low price to TBV.

Ben Graham said he averaged an annual 20% return investing on net nets for around 30 years. The backtests he performed in the ’70s confirmed his prior experience.

Joel Greenblatt, Richard Pzena and Bruce Newberg published a paper in 1981 concluding that a group of net nets returned a 40% CAGR for the period studied (1972 to 1978).

But, aren’t net nets a thing of the past?

There are a handful on the US stock market right now, that’s true. But in Japan, the UK, and other European markets, they’re alive and well.

At Net Net Hunter, we study a list of around 1,000 net nets that appear each month on those markets. We screen the raw list and send a monthly Shortlist to our members to save them hours of work.

If you want to learn more about net net investing strategies, the academic research behind them, and leverage the knowledge of other members, join us now!

Start putting together your high quality, high potential, net net stock strategy. Click here to get free net net stock checklist.

Article image (Creative Commons) by Slon Pics, edited by Net Net Hunter.